Bonds rallied yesterday on the back of disappointing US economic data, though the moves especially in Europe were not that big. The US 10-year yield fell by around 4bp, while the German 10-year edged lower by only 2bp. Italian bonds continued to perform, and the 10-year benchmark yield fell below 3.60%.

Weak US data is set to continue for now, and be it due to bad weather or not, there is a limit to how much the bond markets can stomach on the weather argument. It is thus hard to see any bigger rise in bond yields, before US data picks up again. In the near term, the data looks likely to continue coming in on the weak side, which also applies to today’s housing market numbers (see more below). Bond yields are thus likely to fall further today.

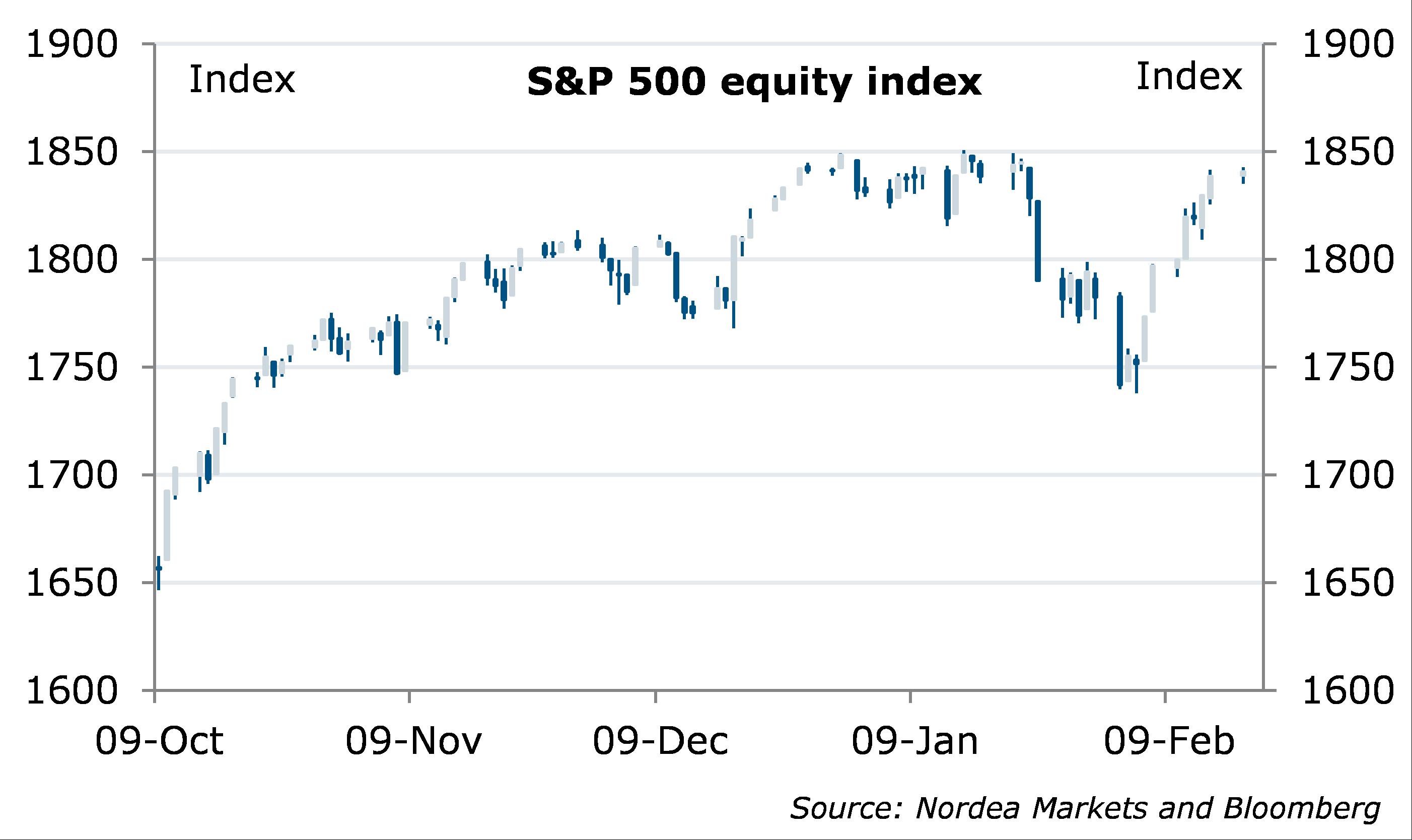

Equity market sentiment was not hit much by weak data. S&P 500 closed the day up by 0.12%. Asian equities are trading mixed this morning, while Europe is set to open slightly down. Continued weak data, especially as S&P 500 is again close to its record highs, could easily put some pressure on equity prices again.

US home builder confidence plunges – more than weather at play

The US NAHB housing market index surprisingly plummeted from 56 to 46, the biggest monthly drop seen in the history of the series (data from 1985). The slump was no doubt affected by weather, but also continued concerns over the cost and availability of labour and lots burdened confidence. The clear fall in the expectations index also suggests weather was not the only factor explaining the drop. The outlook for the housing market has thus been dented to some extent.

The New York Fed manufacturing index, the first one out of the regional manufacturing confidence indices, plummeted from 12.5 to 4.5. However, this only reversed part of the advance seen in January, and the latest value remains the second highest reading in five months. Overall, not a good start for the regional indices, but not that big deal either, considering the volatility in the indicator. The Philly Fed index will be out tomorrow.

A rise in US minimum wage to cost 500 000 jobs?

The Congressional Budget Office released its estimate of what the consequences of Mr Obama’s plans to raise the federal minimum wage from USD 7.25 an hour to USD 10.10 would be. The central estimate would be a loss of 500 000 jobs by the second half of 2016, with a likely range of a slight decrease in jobs to a loss of a million jobs. A more moderate increase to USD 9.00 would cost 100 000 jobs in a central scenario. However, in the USD 10.10 scenario, overall real income would rise by USD 2bn.

With House Speaker Boehner, among others, opposed to raising the minimum wage, an increase is unlikely to take place at least with the current composition of Congress, but Democrats could push such a measure forward on a state-level in several states.

Fed minutes and US housing market data ahead

Today’s data highlights include the US January building permits and housing starts as well as PPI for the same month at 14:30 CET, while Fed minutes will be released at 20:00 CET. Bad weather could easily have affected the US housing market numbers more than expected, causing another disappointment, while Fed minutes will likely illustrate the Fed will not deviate easily from the path of moderate tapering steps.

In Europe, Bank of England minutes will be released at 10:30 CET, while China’s flash manufacturing PMI will be out early on Thursday (at 2:45 CET).

In central bank speeches, the Fed’s Lockhart will share his views at 18:15 CET, Bullard at 19:00 CET and Williams at 1:00 CET (early Thursday).

Dutch 30-year launch not particularly impressive – Germany to sell 10-year bonds today

The Netherlands sold EUR 3.7bn of new 2047 bonds, while the order book amounted to EUR 5.9bn. This was less than the EUR 5.2bn placed in the previous 30-year bond launch in 2010, and the demand was not particularly impressive. The final spread amounted to 20bp vs DBR 2.5% Jul 2044 compared to the initial guidance of 19-22bp.

Germany will continue this week’s issuance today with a EUR 5bn re-opening on its 10-year benchmark.

US equities almost back to record highs

Nordea