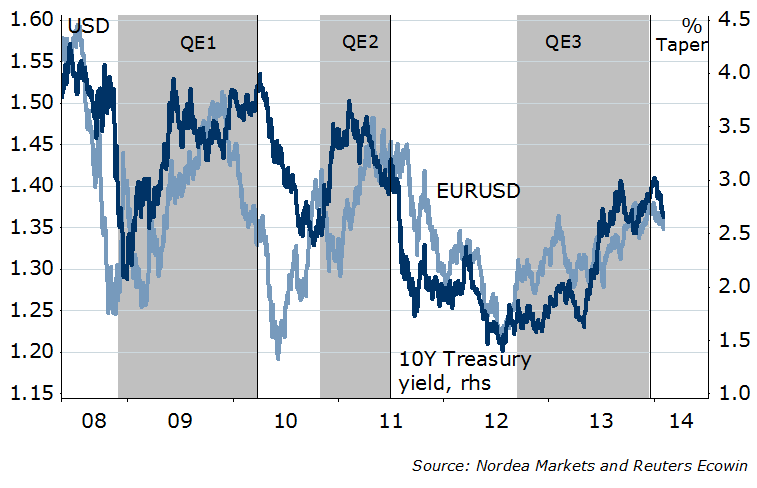

Worringly…more signs of the ”risk on/off” mode coming back over the past week, and most stock indices stuck at crucial supports: below. just. gets. ugly. A little bit of a déjà vu. Last time we saw big “risk offs” when Fed’s QE1 and QE2 stopped (timing was not Bernanke’s skill) – EURUSD down, UST yields down, stocks down, volatility up…

Figure 1. This time is different?

Now, this time is somewhat different: Fed is not quite stopping QE yet, and the European crisis is not rock & rolling. But we have adjustment in Emerging Markets taking place, US debt ceiling back this week, and …some growth worries from, guess who.

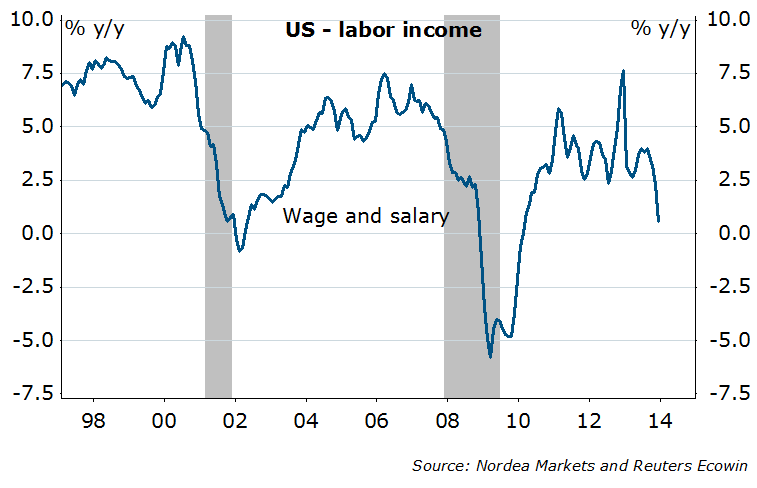

You can blame the weather until you can’t…another batch of weaker than expected data from the US in the previous week: housing market cooling, Q4 GDP composition not that strong, consumer inflation expectations further down, core PCE stuck at 1.1% y/y, wage growth at a standstill (Figure 1), and household savings rate back to 2008…potentially not without some “forced” dissaving. Peak ISM? This week’s highlight number: be ready for a 1-1.5pt drop. Payrolls – the Street expects a payback report (upward revisions) and a healthy 180k January print. Now, it’s a good time to test if the risk on/off is back: good macro news from the US should be bad for the USD, US Treasuries, good for stocks and EMs (and vice versa). The DXY is at crucial resistance levels now: 81.5 is key – if fails here, we will be back to below 80 before long.

Figure 2. Wage-growth-less recovery

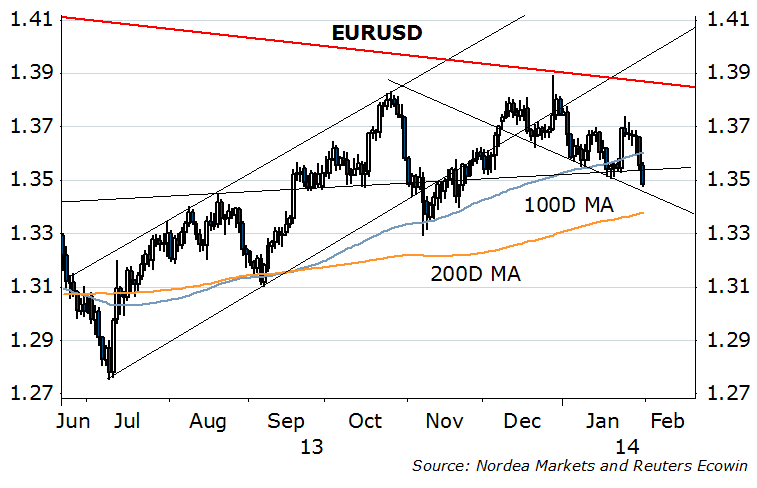

What happened to EUR? Victory lap for the EURUSD bears as they jumped on it crushing the 100D MA last week. Not a huge surprise – end of month, ahead of ECB. Will this time be different? Nope. ECB won’t cut rates, reasons plentiful: the labour market has turned the corner, the credit impulse turned up and the lending survey tone positive, the PMIs and other sentiment/survey data have improved, market-based inflation expectations are rocks solid even with the softer headline CPI print (energy price actually good news, as Draghi noted). Money supply growth deceleration (M3 1% y/y) is ECB’s cross-check… but those referencing deviation from the old 4.5% M3 growth reference are mistaken: blame the unprecedented low rates and “search for yield”. Keep the EURUSD long (from 1.3450), next support area 1.3380/1.3450 (SL 1.3340, TP 1.3850).

Figure 3. EURUSD crucial support around 1.34…

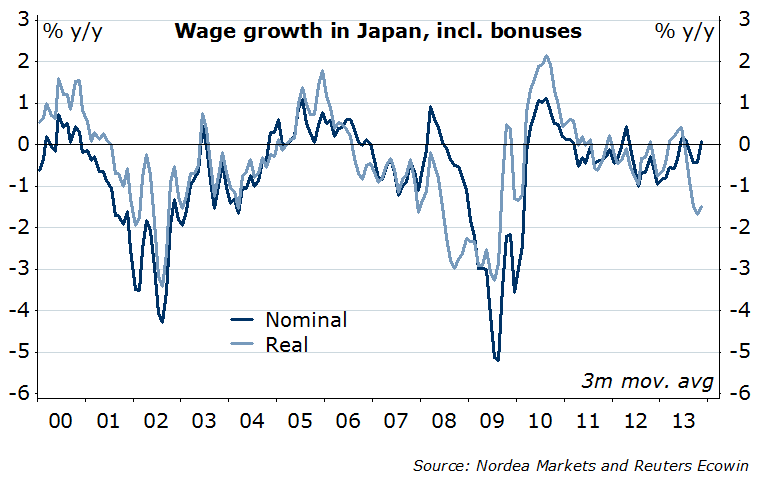

Abenomics has been generous to corporates, with many industrial indicators improving, but not so much to households yet. As we await the 3%-pt consumption tax hike in April, consumer confidence is off peaks and real wages contracting at the rate not seen since Lehman, the reversal of which is needed to prove Abenomics succesful (and thus justify further stock market gains). Took profit on ½ USDJPY short position (from 105) after FOMC last week, seeing the Nikkei and UST 10Y at the trends which yet need to be cracked for the USDJPY to fall to 101.75/80, and if so…then straight to the double digit area.

Figure 4. Abenomics helping households…not yet

Figure 5. Japanese stock market testing the “Abenomics trend”

Everyone is happy with the UK recovery… but in my view the GBP money market rates are still lofty, the GBP is more exposed to more risk aversion and disappointments to data than the EUR. We get PMIs this week (likely unchanged or a bit lower), but even more importantly – industrial production, which has failed to match the fabulous survey data yet. The BoE meeting will likely be a non-event, forward guidance is to be revisited in the February 12th Inflation Report. So far it seems the BoE will shift to the good old central banking, with no hard thresholds, just qualitative guidance maintaining “data-dependency”. (Bo-ring).

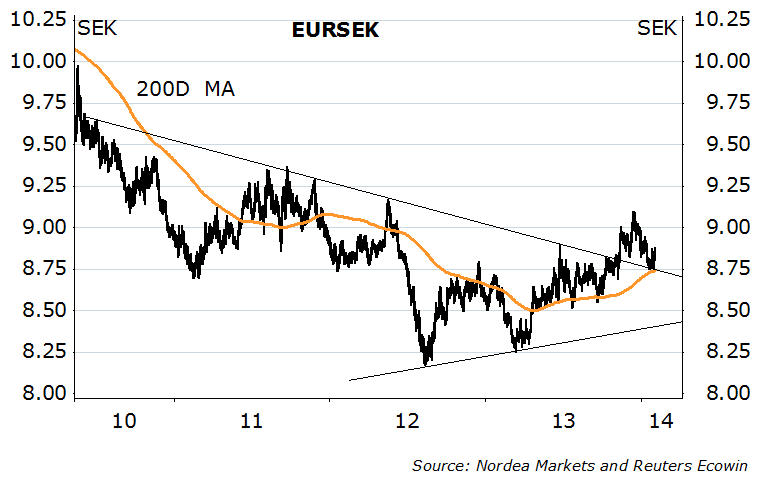

No love for commoditiy currencies yet… the long USDCAD, AUDNZD and NZDUSD short are on the right track. The RBA is not expected, neither priced, to move rates this week, and recent data suggests the AUD weakness is working its way to economy (inflation, business conditions, credit) – and justifies “on hold” stance. The NOKSEK short has reached another milestone too – the dip under the 1.04 area opens a new door toward the parity…but home prices are key key key data point this week (main source of NOK weakness over the past 6M). Separately, though, I recommended a tactical long on EURSEK last week, as the momentum turned positive and the long term downtrend has been rejected…(NB: against our official view, so blame just me if goes wrong).

Figure 6. EURSEK re-tested the downtrend…in vain

Nordea