As the year and approaches, FX volatility should come down. This week – EMU industrial vs US retail sales data, but China will drive the sentiment near term – global growth momentum turning?…

It is very strange to see the volatility increasing toward the year end. Hence the continued USD rise.

Figure 1. Tailwind for USD

…The stock price volatility, however, has fallen in recent weeks, so has the rates volatility, and I would rather bet on the FX fall converging to it, rather than the other way around.

The recent rise in volatility may have been due to the fears of recession, which, I argued last week, is NOT what is likely to happen. On the contrary, betting on recovery is a better risk-reward. Japan and Europe are turning the corner in Q4, and still have a catching up with the US and UK to do in H1 2015. More evidence? Last week: better CEE PMIs, strong German new orders data. This week – likely solid October IP data. Hence the summary of the ECB meeting last week: Buy. More. Time. European currencies should benefit. The EURUSD major trend at 1.2200/50 remains key support.

Just like a dream, was the US payrolls report on Friday. Wage growth picking up may be a signal that the US Treasury longer yields have bottomed. Retail sales is this week’s highlight. Last month was very strong, and there is reason to believe it will be solid too. Stronger household consumption should see trade balance widening more (last week reported larger than expected in October)…not good for USD. One fly in the ointment: still weak mortgage lending data, suggesting household deleveraging not quite over yet.

Figure 2. Energy exports not enough

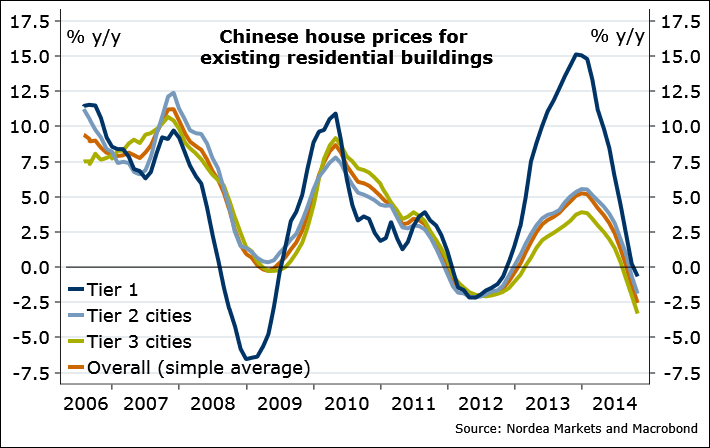

A bunch of Chinese data will be week’s focus. Fingers crossed: better export, retail sales data likely. But all eyes on the housing market in coming months. The housing market slowdown, major headwind in 2014, should be supported in 2015 by recent government measures and the PBoC in particular – worst case, a RRR cut.

Figure 3. China’s housing market cycles – time for a swing up

Keep chasing AUD, NZD, NOK vs USD, I said last few weeks, and still do, think we are up for a lasting turn up in December. Norges Bank meets this week: they, too, must be surprised by NOK weakness (almost 8% than forecast!), balancing the need to cut rate path. The RBNZ meets this week, nothing is expected nor priced in, but they are well known for their word power. Whatever it takes – NZD too strong. Meanwhile, more than a 25bp cut priced in from the RBA within a year. Better news from China will benefit AUD more. The AUDNZD supported at the trend at 1.076, be long, as long as above.

Last but not least, the SNB, not buying gold, but probably thinking how to avoid buying more EUR too… It’s not the baseline they will act pre-emptively, but with the EURCHF stuck on the floor, I wouldn’t be surprised by a rate cut as early as this week. The EURCHF long would perform in the recovery scenario in 2015 anyway, so positioning for upside is a no-brainer. 1.30 coming.

Nordea