Even though oil price fall feels like 2008, it is not, thus consequences will be different. Liquidity is back this week, just as key events – ECB and, expectedly, blowout-payrolls…

It is a coincidence that the oil price peak this year, followed by the sharp drop, happened in the middle of the year – just as in 2008. But in contrast to then, the decline is shallower, and it was not preceded by the rapid rise, which, arguably, was one of the factors pushing the world toward recession back then…

Figure 1. This time is different

The economic backdrop is much better now, as the bubbles the major economies had back then have been deflated. The US ramped up oil production. And cyclically we are beginning to see more signs of the growth momentum picking up in H1 next year. In particular, consumption growth, stronger already in Q4, will be driving global growth in H1 2015, as lower energy prices are helping real incomes.

I had a dream of the US payrolls being just above 400k a few weeks back – a long shot, but consensus for this week is a robust 225k (Nordea’s call is even 275k), which would help the USD on news, but…for how long? If stocks rally. A disappointment from the US front, if any, this week would probably come from the ISM manufacturing, as the US industry lets steam off after some great months.

Softer data from the US, and small positive surprises from Europe are sufficient to support the EURUSD (Figure 2). E.g. last week’s euro area money, economic sentiment data, pointing to a turn up in early 2015 (Figure 3). This remains one of tailwinds for the EURUSD short term, in addition to the seasonal factor: December tends to be a bad month for USD. Just. Technically the 1.2250, multi-year support level, remains key on the downside (if we get that 400k US payrolls report…).

Figure 2. Relative macro surprises – tailwind

Figure 3. Euro area – turning point near

There is no doubt that ECB has moved toward sovereign QE. But there is no doubt, also, that they are not as unanimous as they claim. Just as, for example, Constâncio defended the sovereign QE last week, just another board member expressed her doubt (I agree). But I guess Draghi’s latest words summarize the baseline for this week’s ECB meeting: “time is needed for the positive effects to fully materialise”. Pretty much everyone expects sovereign QE from ECB in H1 2015. Beware. Also, of the impact on the currency from any expansion of QE – too many believe it’s negative.

It is beyond me the moves in commodity FX, and some of the majors trading last week made you wonder, is there any liquidity in global markets?! Maybe the US holiday week exacerbated the swings. The oil drop triggered the stops. But it does seem that the Brent oil should stabilize around USD 70-72/bbl, worst case USD 62/bbl, which finishes the decline from the rising wedge break. Chase the AUD, NOK, long, and relative terms, go for the CADNOK decline: Bank of Canada meeting this week, and I simply don’t see why the Market should be pricing in a cut from Norges Bank vs neutral BoC.

The Bank of England has been watching global events with horror, it seems, and Carney’s recent comments indicate that global factors play a big role in keeping them on hold. No way they want to front-run Fed. No reason to change that in this coming week’s meeting: 7-2 on hold. No comments. Keep GBP short vs EUR, SEK.

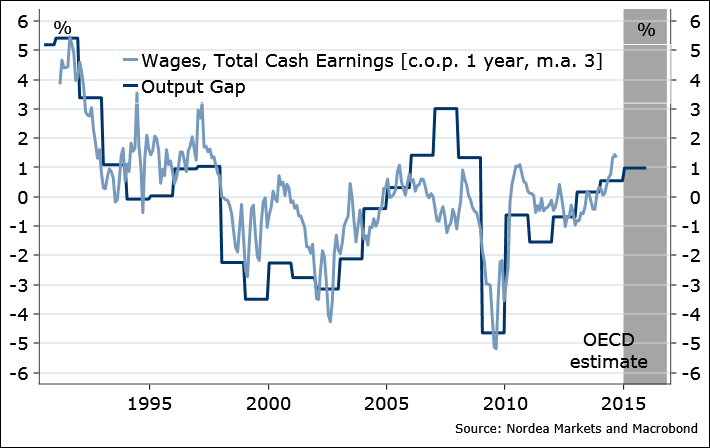

Japan, which was disappointing over summer, looks like ready to strike back in Q4, judging from most recent data, including last week’s industrial production report. If we are to see improvement in global growth outlook, remember, Japan has the output gap closed already, thus wage pressure must be genuine. What is good for Japan – is bad for JPY. Amen.

Figure 4. Wage inflation is back

Nordea