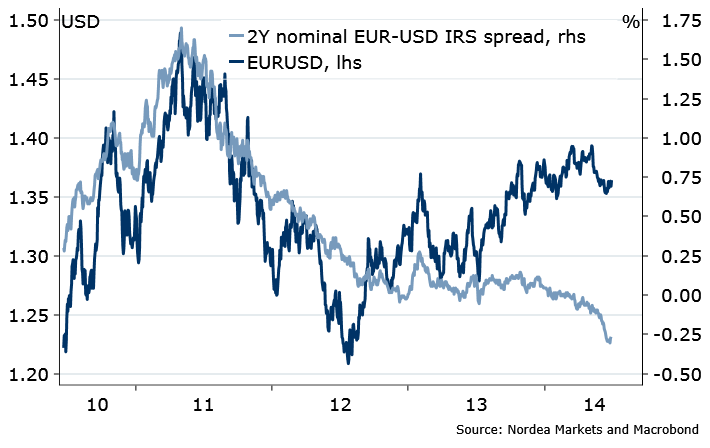

What is the most commonly used reference for the currency “fair value”? The interest rate spread, of course. Many have been puzzled by the fact that the EURUSD has deviated so much from the short term interest rate spread since 2012. It seems, the EURUSD is simply too high!

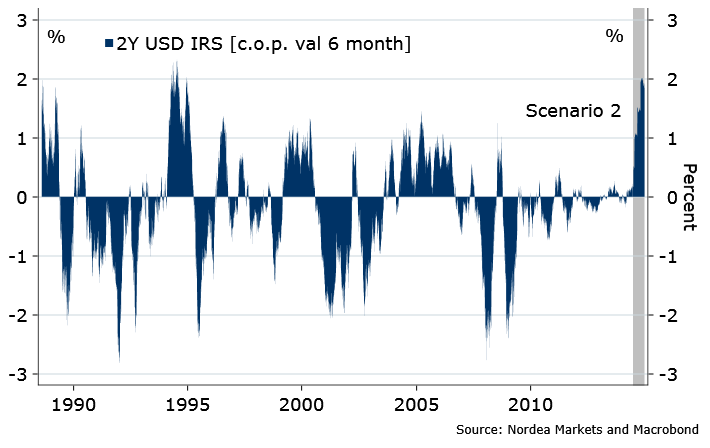

Figure 1. ???!!!

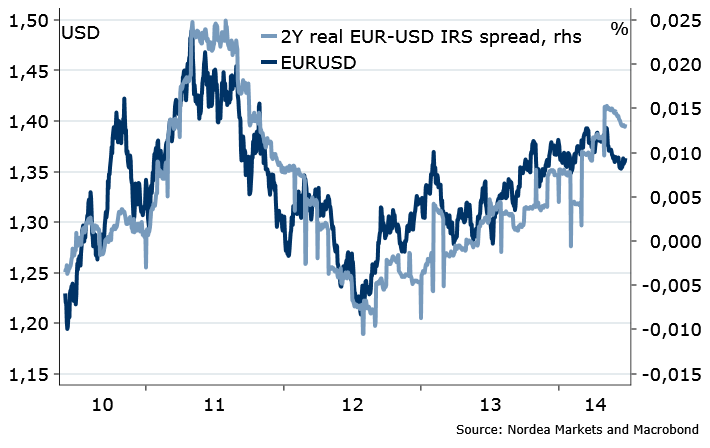

But economics teaches us (still), it’s not just the NOMINAL, but the REAL interest rates that matter (purchasing power parity, PPP). That is, higher relative inflation hurts the currency value. And thus disinflation has actually benefited EUR a lot. Compare and contrast the graphs above, and below.

Figure 2. Aha!

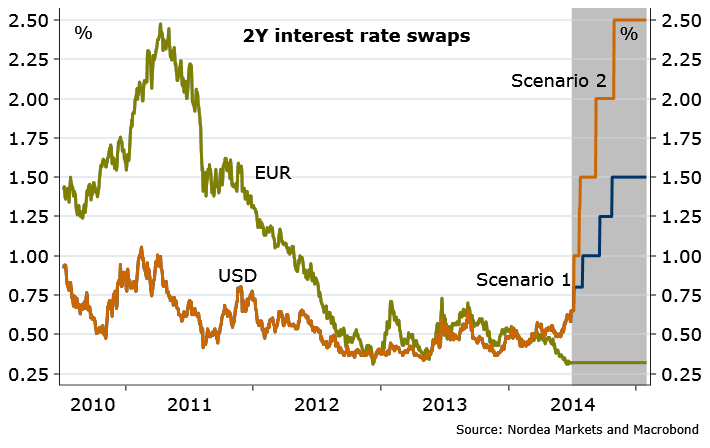

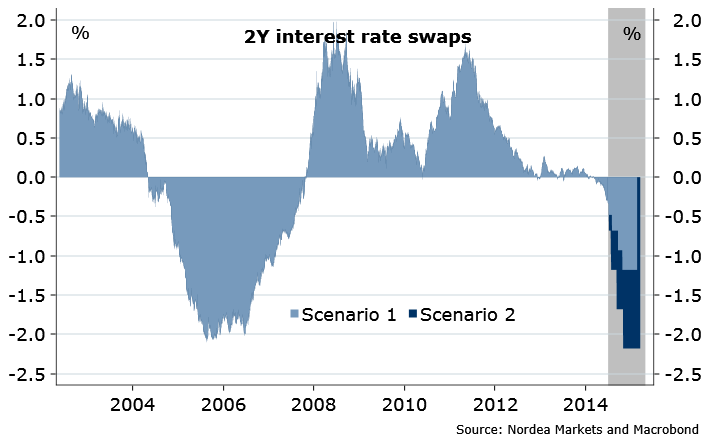

Sharply higher shorter USD rates are not imminent, if you ask me, after Yellen’s latest blessing. But imagine, I am wrong. Imagine, those who say Fed is behind the curve are right, and the USD short term rates are about to explode. Imagine, the EUR rates remain stuck at where they are, and USD 2Y IRS rises by 100bps, or even 200bps by year end. How would that look?

Figure 3. Let’s assume…

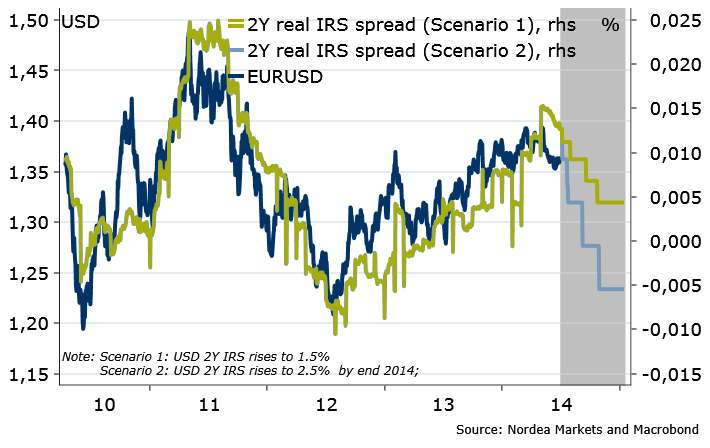

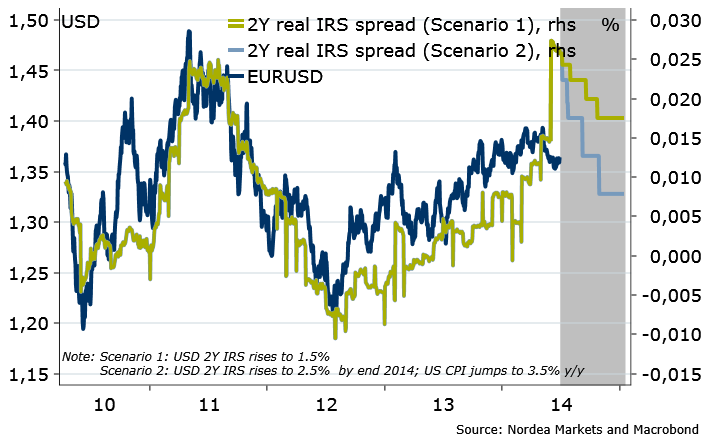

And now see what the above used chart (Figure 2), with the real EUR-USD rates spread, would look like…

Figure 4. Worst case for EURUSD under USD rates shock

Yes, the EURUSD would be lower, but only somewhat. But what is the probability of the USD rates event like this? It would be a similar 6M shock as during the surprise Fed hike / bond crash in 1994 (Figure 5). And the EUR-USD rates spread would be largest since the euro introduction (Figure 6).

Figure 5. But…is that USD rates shock likely?

Figure 6. …Really?

But now, to the more important part. I haven’t touched inflation assumptions yet (assumed unchanged at latest values).

Now, imagine the euro zone remains in the close-to-deflation mode, while the US inflation keeps rising (as almost everyone calls it). No, not just marginally, but a lot, to, say, 3.5% (to justify that aggressive increase in short rates). If one then assumes this to happen, even with the aggressive rise in USD 2Y rates scenario, the EURUSD would be… at current levels, or even above, depending on the size of the USD rates shock.

Figure 7. Higher USD rates? Not without higher inflation. But then…

And finally. Who says the EUR rates will remain close to zero for years (current market pricing suggests so)? Can you see the scenario where the US inflation hits 3.5% and USD rates jump, without affecting the EUR rates? Me not. Simply because global macro cycles are related more than ever, and thus the covariation in rates is high (correlation >0.7) due to shared global factors. Last May, the Taper Tantrum, was a good example of this.

So. The euro zone inflation is this week’s focus data point. And with ECB having nailed rates to the bottom… please, BE surprised if low EMU inflation leads to weaker EUR from now on.

Nordea