ECB won’t kill EUR, as capital flow to resume. The USD staged a sharp reversal down last week, and wage growth stuck at 2% suggests – no Fed funds repricing imminent yet, but…

Party like there is no tomorrow. ECB is giving out free lunch for European banks now. Go ahead. Front run.

Figure 1. Because if you do…

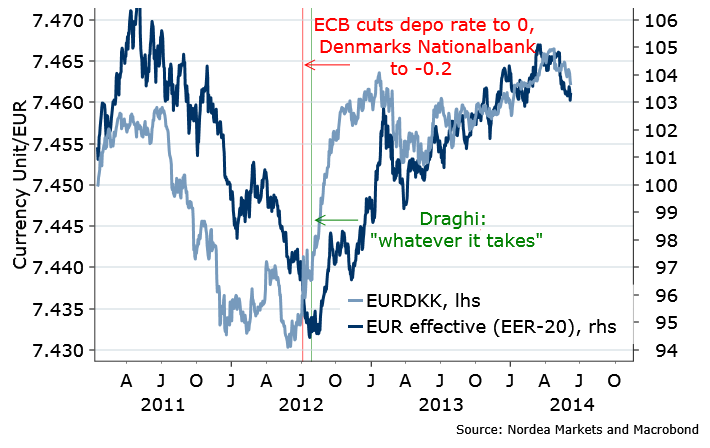

Deposit rate cut? Yes, it’s a cost for European banks, but…seriously: this is just 10bps. And Draghi promised they are not going lower, switching from the rates will “remain at present, or lower, levels” to“remain at present levels”. If you think it will work miracles (weaken EUR), like for Denmark two years ago, – no, it won’t. The DKK did not start to weaken in 2012 due to the deposit rate cut to negative, whatever they say.

Figure 2. It was not DKK weakness. It was broad EUR strength.

Drop it like it’s hot. Massive reversal of USD index last week, with DXY back under the 80.50 – very important. Technically the EURUSD action on the ECB day last week was bullish. It needs to break above the 1.3685 level this week to signal the potential renewal of the uptrend. If above 1.3730, the EURUSD will head back and to new highs (yes, above 1.40) – my best guestimate for this summer, still.

Positive vibes from the US too. Friday’s payrolls was spot on, with only highlight: wage growth still stuck at 2% y/y. No Fed repricing. Dot. But in other news, widening foreign trade gap and the pickup in the credit card lending (last week data) hints domestic demand recovering in the Q2. Are the US households really back? Retail sales figures this week will likely signal so. But, hey, what is good for the US economy, is not good for the US currency, history teaches. The widening trade balance was, actually, one of the reasons people were selling USD before the Lehman…and stopped after.

Figure 3. Back to normal? You wish (not)

The UK is still shining. But monitoring the housing market very closely – historically, positively correlated with the currency. If recent history is any guide, expect softening in growth rates soon. Will it be enough to hit the large long GBP positions? Probably not. But the upside is limited, and any increase in volatility, or sharper change in global rates, would do the trick. This week’s highlight – labour market report – where, most importantly, earnings growth is likely to print lower (base effects) to just above 1% y/y – and away from BoE’s target of 2.5% for 2014. Keep the EURGBP long, forming the base here, and the GBPSEK short, finding resistance at 11.20.

Figure 4. Enough is enough

Commodities front is still doing ok – apart from South Korean data, the Q2 macro looks better most places. Thus longer rates, especially USD, could start trending higher from here, hurting commodity FX. Last week I recommended long EURNZD (longer horizon), target 1.68, in addition to the strategic AUDNZD long. Tactically, the RBNZ meeting this Wednesday, a rate hike is widely expected and priced in, but with the recent developments in housing market inflation and the NZD strength, there is a larger than 50% chance the RBNZ will remain on hold. And expect the USDCAD remain in the 1.0825-1.0950 range but…tempting to rebuy again, with a horizon of more than 1 month.

Nordea