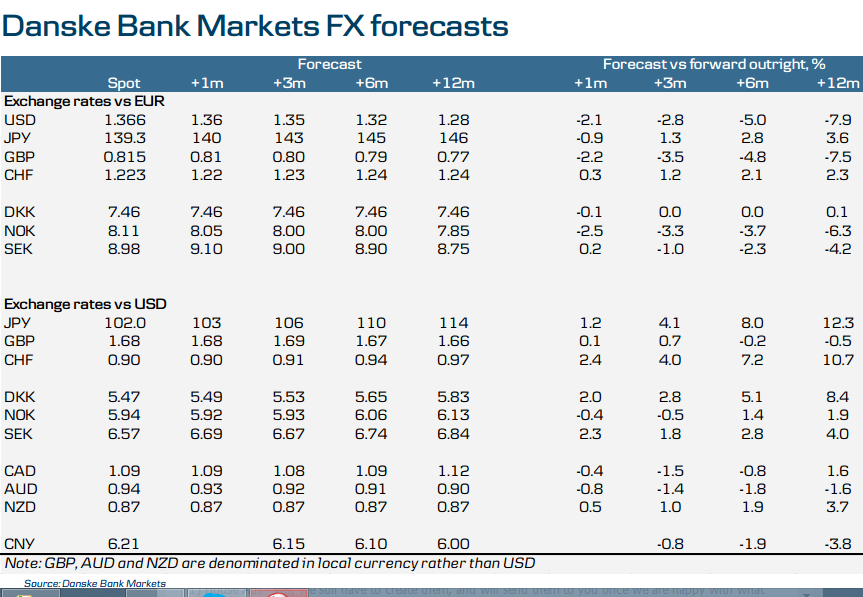

Mario Draghi’s ‘promise’ of further ECB easing in June could very well be the turning point for the euro and in general we have pencilled in more euro weakness to our FX forecast as it now appears more likely that the ECB will actually deliver further monetary policy easing in response to low inflation.

In terms of EUR/USD, the soft rhetoric from the ECB has indeed eased medium- and long-term upside risks to EUR/USD significantly. In addition, we note the downside risks to the US economy have faded following a temporary dip at the beginning of the year and as US recovery is expected to gain pace in coming quarters so Fed tapering will remain on course. We expect the Fed to hike rates in mid-2015 in line with the Fed’s own projection. However, we believe the risk is skewed towards earlier tightening and, as the market is currently pricing in the first hike in autumn 2015 and for prices to increase only very gradually thereafter, we expect a repricing of the Fed funds curve to take place over coming quarters. Hence, we still see potential for a cyclical downtrend in EUR/USD through a trend in relative rates and we now target EUR/USD at 1.35 in 3M (previously 1.40), 1.32 in 6M (previously 1.36) and 1.28 in 12M (previously 1.30).

The combination of the BoE moving towards the first rate hike and the prospect of euro weakness on the back of ECB easing means we expect EUR/GBP to move lower over the coming year. Given that we now expect more aggressive easing from the ECB, we have pencilled in slightly more sterling strength over the next 12 months. We now expect EUR/GBP drop to 0.80(0.81), 0.79(0.80) and 0.77 on three-, six- and 12-month horizons. In particular, on a 12M horizon, we expect sterling to appreciate against the euro as the BoE is way ahead of the ECB in the monetary policy cycle and as an expected stronger US dollar tends to support sterling.

We have kept our USD/JPY forecast unchanged and still target USD/JPY at 106 in 3M, 110 in 6M and 114 in 12M. However, we highlight that weak economic growth has increased the probability of the BoJ easing earlier.

In the short run, further ECB easing is likely to cap EUR/CHF upside and we have consequently lowered our 3M forecast to 1.23 (1.24). In the next six-12 months, however, we still expect EUR/CHF to gradually edge higher towards 1.24 (before 1.25 and 1.26), mainly driven by a reversal of safe-haven flows and an increase in Swiss portfolio investments abroad.