The EUR/USD rate has been remarkably stable so far this year trading mostly within a 1.3500-1.3900 range since the start of the year, (the closing low was 1.3486 on 31st January and the closing high was 1.3934 on 18th March), notes Bank of Tokyo-Mitsubishi UFJ (BTMU).

“Furthermore, volatility has plunged to levels not seen since prior to the financial crisis. 3-month EUR/USD at-the-money implied volatility hit a closing low of 5.89% [last week], the lowest level since August 2007 just before the first signs of the financial crisis were emerging,” BTMU adds.

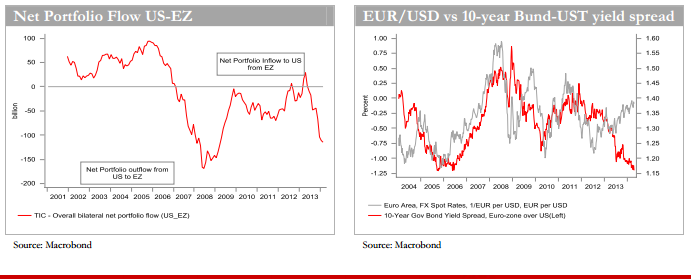

As this stability of the euro versus the dollar at close to levels not seen since 2011 comes at a time when the ECB has been attempting to ease monetary conditions through forward guidance, it suggests that portfolio flows continue to be instrumental in supporting the single currency against the dollar.

EZ inflows contrast with US outflows:

“On current available data, the inflows to the euro-zone have been impressive and help explain the resilience of the euro in circumstances of the ECB trying to play up the prospect of easing without actually doing anything. The inflows are all the more impressive when juxtaposed with the awful portfolio flow data from the US.” BTMU notes.

US investor outflows worsens the net portfolio picture:

“Worst still, US investors’ appetite for foreign securities has been picking up at the same time as the US experience weak foreign investor demand for US securities. When US investor flows are included, the overall portfolio flow was a net outflow of USD 56.9bn on a 12-month basis in February, less than the USD 157.2bn outflow recorded in January, which was the largest 12-month net portfolio outflow on record going back to the start of the TIC data in 1977,” BTMU adds.

Looking ahead, 2 arguments for a shift in flows picture:

“Firstly, there may well be further demand for periphery debt from abroad but the value aspect of this trade is surely getting stretched at this stage. Ireland, which was bailed out just over three years ago to the tune of about 40% of GDP, now has 10-year government debt yielding a mere 16bps over UST bonds. The Italian premium is just 40bps and Spain’s is 37bps,” BTMU argues.

“Secondly, the end of QE tapering will bring into sight the first stages of actual rate increases in the US. TIC data reveal that the four largest spikes in UST 10-year bond yields from 1990 through to start of the financial crisis (Sep ’93-Nov ’94; Jan ’96- Aug ’96; Jun ’05-Jun ’06; Sep ’98-Jan ’00;) drew substantial capital inflows from abroad,” BTMU adds.

All in all, what does this mean for EUR/USD?

“So with the periphery spread compression perhaps close to completion and with the Fed QE coming to an end, we expect the UST-German bund yield spread to start playing a more important role in pushing EUR/USD lower through the second half of the year, toward our year-end target of 1.3000,” BTMU projects.