From thinking 360 degrees…to “thinking hard” now: ECB. No QE in the near term, but some hints about the horizon. If ECB does QE at some point, how would EUR react?

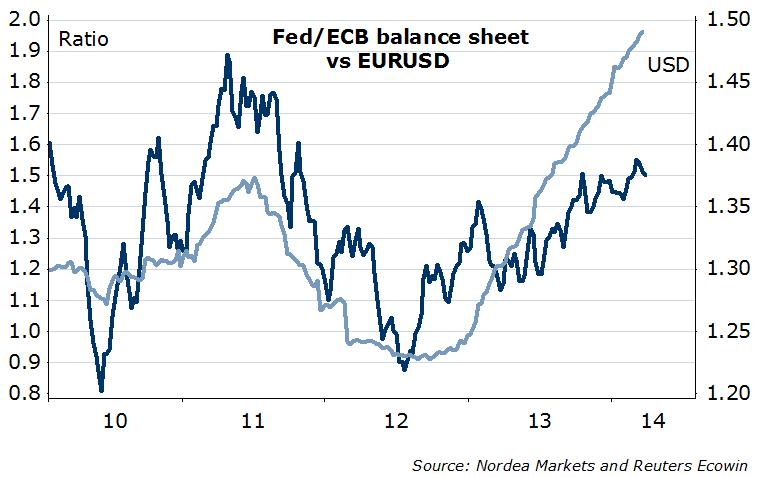

Well, looking at the famous chart below, it is natural to conclude: EURUSD could finally go down, if ECB just does hard enough…

Figure 1. Uncommon sense

…but here comes the “but”. Or a few.

Firstly, the relationship above is not exactly logical. It’s worked by psychology, or just coincidence. If you are familiar with the monetary models of exchange rates, the base money expansion shouldn’t cause currency to weaken. Only the “inflationary” private money supply (banks vs private sector), not the base money (banks vs central bank), expansion, should be associated with currency weakness. (No more theory below, I promise).

Secondly, USD and JPY may have been exceptions. We know that the US Fed’s and BoJ’s QE has been associated with weaker USD and JPY. But the only reason why it happened is because both have a history of being treated as funding currencies, hence, “safe haven” currencies when the risk aversion strikes. What happened with the QE in US and Japan is exactly that: stock markets went ballistic as the “safe haven” currencies weakened. Now, is EUR a “safe haven” currency more than the USD? My impression, we are not there just yet, as the prevailing perception is that the euro zone is still more vulnerable to financial shocks (and probably is).

Thirdly, it depends on what type of QE. Draghi was explicit last week in that the euro area is institutionally different from the US – ECB’s QE would likely look different from Fed’s and BoJ’s. Most likely, it would be a targeted LTRO, similar to, BoE’s funding for lending, the hint on that was the last sentence at ECB’s press conference (a new paper on this is coming at IMF’s spring meeting starting next weekend). It is not certain how much such a scheme will be used (what impact on ECB’s balance sheet). In any case, note that the GBP strengthening since last year has been consistent with the BoE running the programme – and they are still running the scheme for SMEs.

Figure 2. Now look at history of ECB’s policy during crisis…

Fourthly, remember the history of ECB action. Chart above. ECB effectively did a lite QE, or LTRO, in 2011 and 2012, and then hinted the OMT. It was definitely not what drove the EURUSD down – rather, eventually up, on declining rates (credit spreads) and improving confidence. My thesis is, it is actually not important as who is doing QE: as long as it is improving growth expectations, the USD will weaken broadly. That’s consistent with the history of the USD (usually strengthens in recession, not growth regimes), and the chart below. QE from Fed has led global yields up, stocks up, EURUSD up, all likely on better growth expectations.

Figure 3. Higher USD rates – weaker USD

Fifthly, there is limited impact through rates. If ECB does a conditional QE down the road…first impact could be negative (signalling effect), but ultimately, the EUR rates are already so low that the size of the effect must be limited. As regards the interest rate spread, note, also, that the rise in the USD-EUR short rates spread (e.g. 1y1y) has been consistent with the EURUSD going up since last summer… just like with the UST 10Y yields when the Fed was engaged in the QE, the chart above. And look what happened intraday last Friday after payrolls – USD yields went down together with the EURUSD.

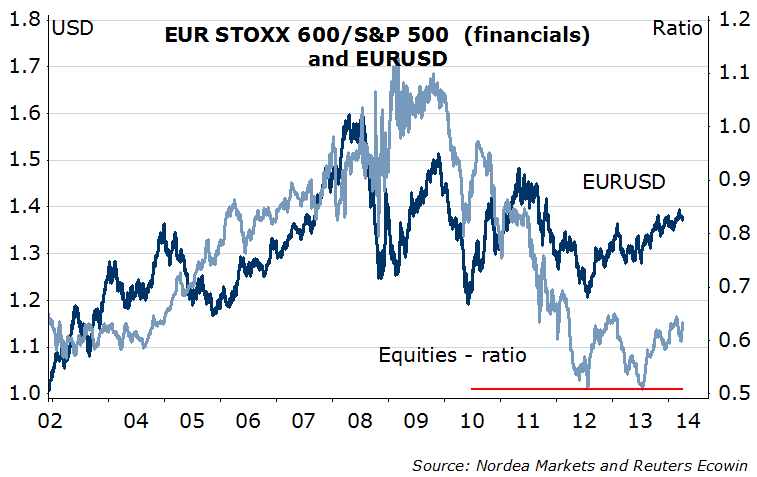

Sixthly, ECB QE should boost risk appetite. And it should lift the stock markets, encourage further capital inflows to the euro zone. We have seen big increase already: the EMU M3 growth recently has been primarily driven by changes in net external asset position. Now that the peripheral bonds have largely played out, equities are still relatively attractive. And it may be just the beginning: the European stocks are still cheap relative to the US, in particular the financials (e.g. P/B ~0.8 vs ~1.3 for US). European bank asset quality review this year would be a confidence card – potentially stronger, if followed/accompanied by some sort of ECB QE.

Figure 4. European financial stocks catching up

Seventhly, everything is relative, especially so in the FX world. Say, you are a firm believer in the Figure 1, and think it will keep working. Now note, inflation trends have been similar in both the US and EMU over the past few years. In the scenario where the ECB launches QE, ask yourself, what will Fed will be doing? And the answer, with some lessons from history, I think, is quite obvious: definitely. not. less.

Figure 5. No decoupling

“

My biggest fear is actually to some extent reality” – Draghi said last week. If reality is bad, or especially if it gets worse, then changing it, with additional targeted monetary easing from ECB, would likely be positive: for risk appetite, for growth, for EUR.

Nordea