More relief coming? Three things: the US, and in particular China economic surprise indices are at record lows; positioning in the cyclical commodity currencies is turning from deeply oversold levels; and … just weather.

FIgure 1. Enough is enough? Bad news.

AUD still the favourite: the central bank’s tone has become more mild (last week’s Steven’s speech), data stabilizing or improving, and the RBA will remain on hold this week. Keep the AUDNZD long, for a move toward 1.1050. The Canadian data, dismal lately, could actually be good enough this week – potential rebound in formerly weather affected numbers like GDP, jobs, as well as exports, in CAD favour. Both CAD and even NOK, both medium term shorts, can perform further as Emerging Markets FX gain, closing the volatility gap with the majors from above. This, maybe after a brief break, could extend for at least a few weeks.

EURUSD weakening ahead of the ECB meeting? Been there, done that. And then… sharp spikes during/after ECB meeting. Euro area inflation low, and will likely print 0.6% y/y if not to 0.5% y/y this week. But: 1) this is not unexpected – base effects from early Easter (ECB knows it, will downplay) 2) March will be the cycle lows, up from there (ECB likely expects it). So, no – no action from ECB this week. Lower inflation not necessarily bad for currency, because with it we get higher real rates. But, even more importantly, higher real purchasing power for consumers. Could the latter be reason for, as we learned last Friday, “improved sentiment was driven by markedly more confident consumers. “ ? Why not.

Figure 2. Pent-up demand for “more stuff”?

All the talk “against EUR” last week (headlines somewhat cherry-picked by media) was just allusion to “hypothetical” scenarios, as ECB’s Weidman put it. The conditions much change first – cyclical data to worsen, yields to pick up – for the ECB to get seriously worried. Keep the EURUSD long (entry 1.3450) for a move to 1.42, take early profit at 1.3630, and potentially short.

US inflation is higher, but slightly so, with the Fed-preferred PCE core at 1.1.% y/y, headline falling below 1%… doesn’t make Fed happy. Payrolls this week: 200k is the consensus. Around this number, or slightly higher, should be good for risk sentiments and bad for the USD. No, the Fed funds futures rate grinding higher is not a recipe for the broad USD strength. Only that, consistent with a spike in volatility / drop in stock prices, would cause the USD strength. Alternatively, a very bad (closer to 100k) payrolls, which would make us remember the “R” word, would make the USD gain.

Figure 3. Spot the decoupling

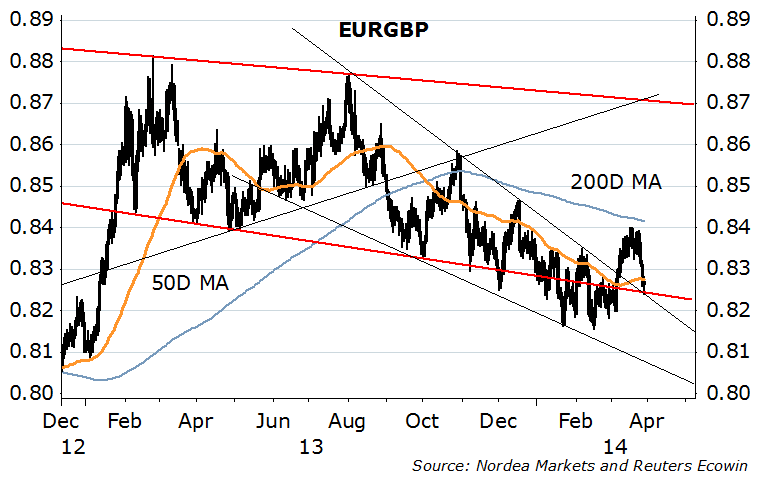

UK just keeps doing this thing – surprising on the upside, also with the retail sales, consumer confidence improving, house prices increasing. But the PMIs out this week, will likely see a small drop. The GBPUSD has a high chance to move back to short term, maybe even 1.6800 (trendline)…but the EURGBP should recover after last week’s drop. Keep the tactical EURGBP long (0.8207), but close stop/loss at 0.8150. Last attempt for now.

Figure 4. Support line around here

Getting a tax hike on a Fool’s Day…that’s Abenomics. Last week Abe’s economic advisor Honda hinted that the BoJ additional easing possible already in mid-May. But so far it doesn’t seem the BoJ is excited with more QE soon, discussing drawbacks. Like the fact that the Japan’s real wages are contracting at the rate of 1.5% y/y, consumer confidence dwindling, and …consumption itself 2.5% y/y down in February. With higher inflation you buy more stuff (fine print: if wages are growing too). Keep the strategic USDJPY short, but tactically be ready for a bounce to above 103 on “less worse” global macro data, notably payrolls. If.

Nordea