Core bonds rallied in earnest yesterday, curves bull-flattened further, intra-Euro-zone spreads widened and equities took a beating. In other words, flight-to-quality was the name of the game, as worries related to China and Ukraine dominated.

The US 10-year yield plunged by almost 9bp, while the German 10-year one slumped by some 6bp, just hitting the lowest level since last July. The next support level for the German 10-year yield is located at last July’s lows at around 1.50%.

Equities took a beating on both sides of the Atlantic. S&P 500 suffered a loss of 1.17%, while Asian equities have been under broad pressure overnight (Japanese equities are down by more than 3%).

With a referendum in Crimea still planned for Sunday (see more below), the cautious tone is likely to prevail today, bonds are set to remain supported and equities under pressure. However, the magnitude of today’s moves in the bond markets is likely to pale in comparison to what we saw yesterday.

Draghi trying to talk the euro down

The ECB’s Governing Council has clearly become increasingly worried about the strength of the euro. Yesterday, it was Mr Draghi who tried to talk the currency down, and did actually manage to put at least temporary downside pressure on the euro. He said the ECB’s forward guidance created a de facto loosening of policy stance, and the real interest-rate spread between the Euro zone and the rest of the world would probably fall, putting downward pressure on the exchange rate, everything else being equal. He added the ECB had been preparing additional non-standard monetary policy measures to guard against a contingency of deflation risks increasing. The ECB thus clearly remains tilted towards further easing, and if it does not manage to talk the currency down, it may have to follow words with action.

China worries catching increasing attention again

Following a weak batch of disappointing economic data, Chinese Prime Minister Li Keqiang warned China was likely to see a series of defaults, as the government accelerated deregulation, but ensured the government would make sure such defaults would not pose a threat to the financial system. On growth, he said the government was not preoccupied with GDP growth, and would be satisfied with reasonable range of growth as long as it produced a sufficient level of employment. The comments on growth suggest China is not fixated in reaching a certain level of growth at any cost, which is welcome news. Going forward, developments in China will receive a lot of attention and risks remain tilted towards further bad news surfacing.

US retail sales rebound – initial jobless claims encouraging

The 0.3% m/m increase in US February retail sales excluding autos was not too bad considering the bad weather, but it followed a downward-revised 0.6% m/m drop in January. There is certainly scope for sales to rebound further in March amidst fewer headwinds caused by bad weather.

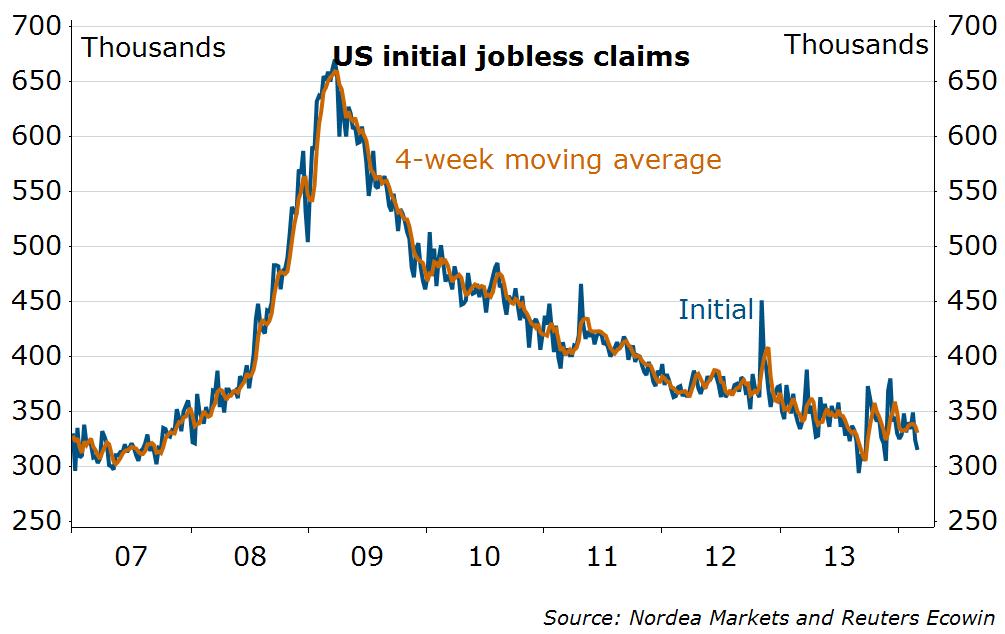

Initial jobless claims data was encouraging, though one should never put too much weight on one week of data. Claims fell from 324k to 315k, the lowest number in six months. This was enough to push the more reliable 4-week moving average to the lowest level seen this year and suggests the labour market momentum is increasing again.

More turbulence ahead over the weekend?

Things could easily heat up further over the situation in Crimea this weekend, as the area is set to vote in a referendum on whether to secede from Ukraine and join Russia on Sunday. A yes-vote would not be a big surprise, but its consequences are less clear and could easily worsen relations between Russia and the US / EU further. The EU and the US have threatened to impose further sanctions on Russia, unless the referendum is cancelled. Safe positions, i.e. government bonds, are thus likely to be in demand ahead of the weekend.

ECB prepayments and US consumer confidence in the calendar

After the pace of repayments in 3-year LTROs picked up to EUR 11bn this week, today’s data will receive more attention again. The numbers will be out at 12:00 CET.

In terms of economic data releases, US February PPI will be released at 13:30 CET and preliminary March University of Michigan consumer confidence at 14:55 CET.

Initial jobless claims started falling again

Nordea