Bad US ISM? Weather. Bad Chinese PMI? New Year. Markets will keep living on the hope that the exogenous factors are to blame for the “soft patch”. That hope will likely keep the sentiment alive, equities, EMs and rates range/higher/stronger in the coming month – hope dies last. In previous years, it was China and euro area growth concerns which took the risk appetite off the cliff…

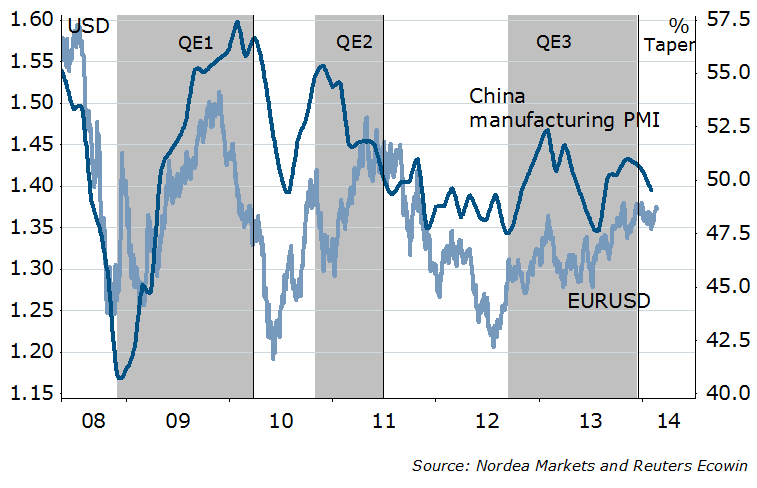

Figure 1. EURUSD. Loves. Growth.

…this time it could as well be the US, given the high expectations for 2014. But for now…Is it worth anything, the US data? Only a bucket of salt.

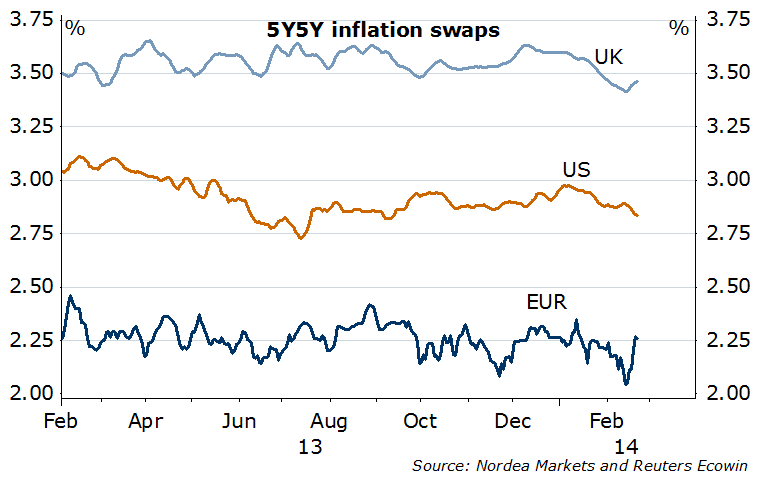

If the risk sentiment holds for longer (assumption), the EURUSD will continue grind higher toward 1.3830, and if that key level taken, to 1.42. Alternatively, stocks fail from current levels this week, and the EURUSD heads down: sell if below 1.3630. At least Europeans don’t need to blame weather! If anything, the opposite – new orders helped by “unusually mild” weather. In a broad global slowdown picture, the euro area looks still decent, data consistent with 1%+ growth, tailwind/lag in this global business cycle. Inflation data is out this Friday, our and the consensus’ call is stable readings (0.7% core, 0.9% headline). What matters for ECB is expectations, which they keep saying are well anchored – after the recent SPF projections coming in line with ECB’s, and break-even EUR inflation declining, but without affecting the long end much. ECB’s Draghi, Nowotny, Praet, Weidmann, – all to hit wires on Thursday, with a likely lacking sense of urgency ahead of ECB’s March 6th meeting.

Figure 2. Steady as it goes – long term inflation expectations

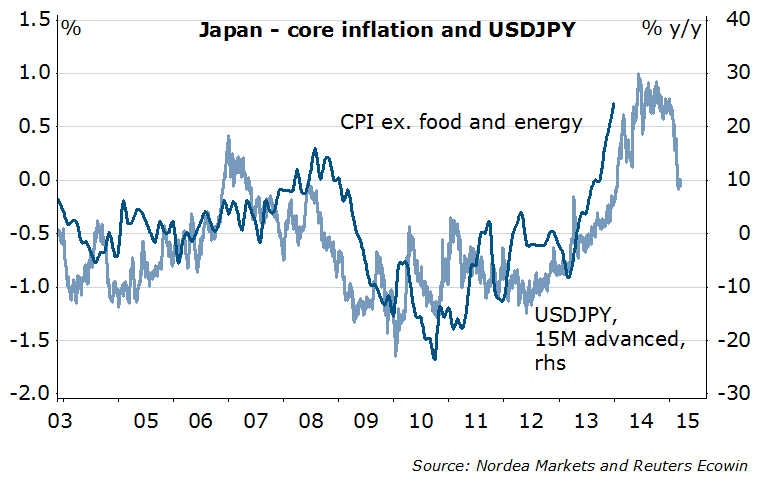

Peak inflation? The Bank of Japan tried to surprise markets with the expansion of Funding for Lending facility last week…but just 1/10th of their QE, not addressing the core of the problem (demand, not supply), thus doesn’t change the big picture. The April VAT hike will introduce some volatility to the economy – hopes for the front-loaded consumption (big ‘?’), followed by the drop. Economic volatility should spill over to currency volatility, in JPY favour. Aside from that, seems more currency weakness is not to be tolerated by the usual suspects. And inflation, a reading of which we get this week, should still be “high”, but…for how long? Hold the USDJPY short, but it could still drift higher (next resistance at 103.40) before it reverts to 101, then crashes to double digits.

Figure 3. Inflation is always and everywhere… a JPY phenomenon

Marking to market, from the Bank of England… referring to Weale’s comment last week on that the first rate hike will come in spring next year, already had been market pricing for some time. Mind you: the guy is on the hawkish side. We do have a few BoE speeches this week, but too early to expect something different from previous week’s Inflation Report. Finally the GBPUSD gave in a little at the end of last week, bearish way, but wouldn’t short yet unless the stock markets resume the decline already this week. The GBP now is the longest long out there, suggested among other things by futures data. Keeping the EURGBP long: once above 0.8300, room for much more (first stop 0.8650). Risk aversion is preferred…thus patience is virtue.

Last but not least… we have a lot of Fed speakers this week, especially on Thursday – Yellen, Pianalto, Lockhart, George, and Fisher; on Friday – Stein, Kockerlakota, Evans and Plosser. Because, you know…

Nordea