Bonds rallied early yesterday, but the direction turned later in the day, partly in response to Fed minutes (see more below). German yields ended the day slightly down, while US yields rebounded (10-year yield up by around 3bp). Intra-Euro-zone spreads mostly widened.

China’s HSCB/Markit flash manufacturing PMI, released early today, disappointed with a drop from 49.5 to 48.3, a 7-month low and the second drop in a row. The fall was not positive, but like most of recent Chinese data, may have been affected by the Chinese New Year.

As risks are tilted towards further disappointments in economic data today (see more below), bonds are set to perform again.

European equities ended yesterday with modest gains, but in the US, S&P 500 finally fell by 0.65%. Asian equities are also trading mostly with losses this morning and Europe is set to open clearly lower.

Fed not about to change course

Minutes from the Fed’s January meeting further supported the notion that the Fed is determined to proceed with its moderate tapering. There was a lot of discussion around how the Fed could change its forward guidance, but no decisions were reached on the topic. A few participants even raised the possibility that it might be appropriate to increase the federal funds rate relatively soon, but these participants are clearly in the minority.

There has been plenty more bad data since the Fed’s January meeting, but more recent comments suggest the Fed remains comfortable with its tapering plans. Atlanta Fed’s Lockhart (non-voter this year) said yesterday that the outlook remained positive and as long as it remained solid and would not deviate dramatically from the Fed’s expectations, he would expect tapering to continue. San Francisco Fed’s Williams (non-voter) echoed such comments, saying the hurdle for changing the current tapering pace was pretty high. The comments from Lockhart and Williams thus suggest that the recent weak data releases have not caused big worries inside the Fed either.

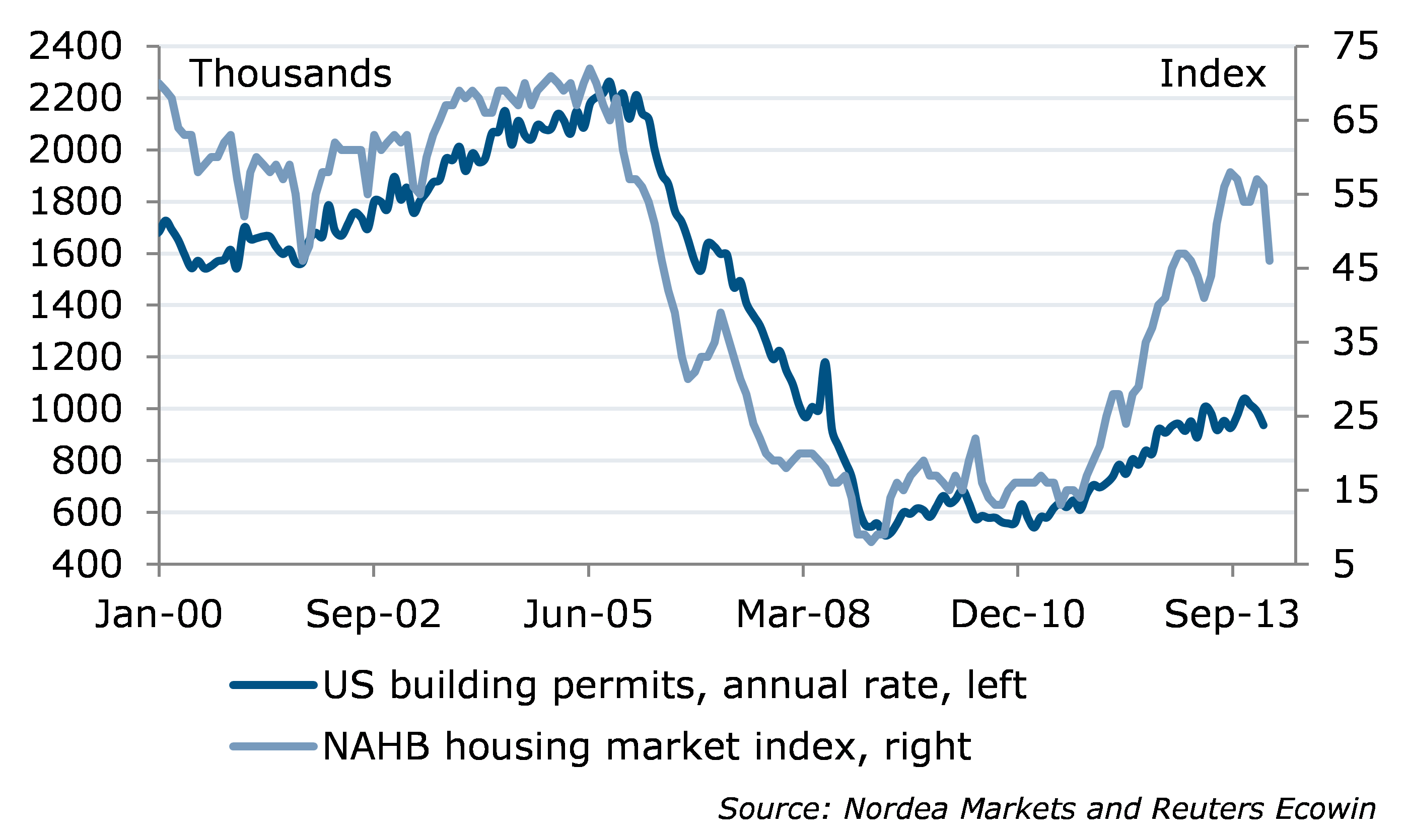

Weather, weather, weather

Bad weather spoiled yet more data releases yesterday. January housing starts plunged by 16.0% m/m (though from upward-revised December levels), while building permits plummeted by 5.4%, both clearly weaker than expected. Weak data is likely to continue in the near term. The numbers were blamed once again on weak weather, but it may not account for all the weakness in the data. The housing market thus appears to have lost some steam.

Austrian ratings under pressure – a risk for Austrian bonds

Austria has been under pressure lately due to the fate of the nationalized Hypo Alpe-Adria-Bank. Chancellor Faymann has not ruled out insolvency, while Finance Minister Spindelegger has wanted to keep all options on the table. The government’s plans to create a bad bank to absorb assets from Hypo could significantly boost government debt and put pressure on the Austrian ratings. Moody’s has already downgraded Hypo as well as the Carinthia province, which has given guarantees to Hypo’s bonds

The Hypo case poses a risk for the Austrian rating. Fitch will review its AAA rating with a stable outlook tomorrow, while Moody’s (currently Aaa with a negative outlook) will have its turn next week. A change in the outlook by Fitch would probably not do much damage, but a downgrade by Moody’s could add pressure on Austrian bonds. Austrian bonds thus face some underperformance risks in the near future.

PMI and inflation day

Today’s data calendar looks quite interesting. Expectations are for an unchanged Euro-zone manufacturing PMI reading at 10:00 CET look quite optimistic relative to the recent development in the US and China. The services PMI, in turn, is expected to increase. Risks are clearly tilted to the downside, so bond could easily receive another boost. French PMIs will be out already at 9:00 CET and German ones at 9:30 CET.

In the US, fresh inflation data in the form of January CPI will be released at 14:30 CET, along with weekly jobless claims, while the preliminary February Markit manufacturing PMI will be out at 14:58 CET and the Philadelphia Fed manufacturing index at 16:00 CET. All the US data releases are interesting, but considering the size of the fall seen in the US manufacturing ISM index, today’s confidence numbers are likely to fare at least somewhat better.

In central bank speeches, the ECB’s Constâncio will speak at 11:30 CET.

Sizable bond auctions in store

There will be plenty of action today also on the issuance front. Spain will re-open bonds maturing in 2019, 2024 and 2044 for a combined EUR 4 to 5bn. France, in turn, will tap 2-, 3- and 5-year bonds for EUR 7 to 8bn as well as inflation-linkers for EUR 0.9 to 1.4bn. Finally, USD 9bn of 30-year TIPS will be sold in the US.

More than bad weather?

Nordea