The ECB kept rates unchanged and confirmed its forward guidance – key interest rates will remain at the current level or lower for an extended period. The ECB is ready to consider all available conditions, but is not ready to act at this point.

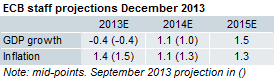

New ECB staff projections showed a fairly low inflation forecast for 2015, which clearly signals intentions to keep rates low for an extended period and signals a wide-open door for more easing in the months ahead in case of new shocks. The projections also showed a downward revision of the inflation forecast for 2014 and a marginal upward revision of GDP growth for 2014.

{kind=link}

On potential new measures

Mr Draghi said that the Governing Council had briefly discussed negative deposit rates. Mr Draghi also said that the LTROs were introduced at a time of considerable uncertainty and worked in that situation. However, the situation is different now and the ECB would need to make sure that such a measure would make its way through to the real economy to do it again. That surely sounds as if the ECB is not ready to do unconditional LTROs. . If anything, any new LTRO is likely to be conditional on bank lending in some way.

Moreover, Mr Draghi did not sound as if the ECB is ready to do another LTRO or to cut the deposit rate in the near future. However, he also said that the level of preparedness is high regarding all tools and he said that the ECB is aware of the risks implied by a long period of low inflation, as expected in the staff projections.

Finally, Draghi repeated that the exchange rate is not a policy target, though the ECB is obviously watching it.

Nothing new on liquidity

The ECB did not announce anything new on money market operations, which could increase money market volatility over year-end, if the ECB does not decide to act later. The ECB may want to wait until after next week´s Money Market Contact Group meeting to decide details, but it would not be the ECB style to wait that long – they have been pro-active on liquidity lately (suspending LTRO repayments during year-end and extending fixed-rate full allotment).

Draghi said that the Governing Council had previously toughed upon the option of not sterilizing SMP holdings, which does not sound as if it is nearby.

Market reaction

EONIA 1Y1Y forwards are up 5 bp and German 10Y Bund yields are up around 3 bp. Higher money market raets has helped push the EUR/USD to the highest level since 31 October. We are likely to see EURUSD at 1.38, if not higher, in the near term.

Nordea