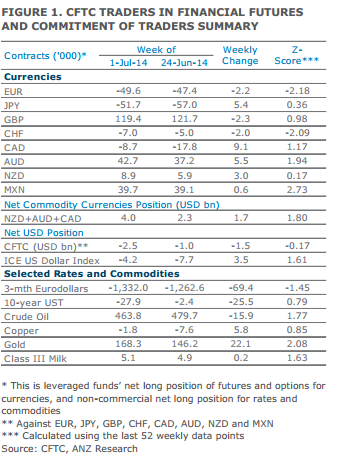

• Leveraged funds increased their net short positions in the USD by USD1.5bn. This comes following the release of final Q1 GDP data showing a much larger contraction that initially estimated. However, the positioning data for the week ending 1 July coincided with the low in the DXY Index, suggesting short covering in the lead-up to last week’s payrolls number.

• The largest weekly positioning shift was in CAD, where short positions were cut in half from 17.8k contracts (worth USD1.65bn) to 8.7k (worth USD0.81bn). This likely reflected short covering, as leveraged funds who a week earlier had increased their bearish bets on the loonie only to see the currency rally, unwind some of those short positions.

• AUD net long positions rose to its highest level since late April 2013 at 42.7k contracts, an increase of 5.5k (worth USD0.6bn). The elevated positioning help explain the sharp decline in AUD following RBA Governor Stevens’ speech last Thursday where he said the AUD remains uncomfortably high and that the market was too complacent about a potential fall in the currency.

• Short EUR positions were increased to 49.6k contracts from 47.4k previously. However, EUR/USD appreciated during the period, indicating that real demand for euros were more than outweighing speculative selling.

GBP remains the favoured currency despite a slight reduction in net long positions. Leveraged funds are net long sterling to the tune of USD12.8bn.

ANZ