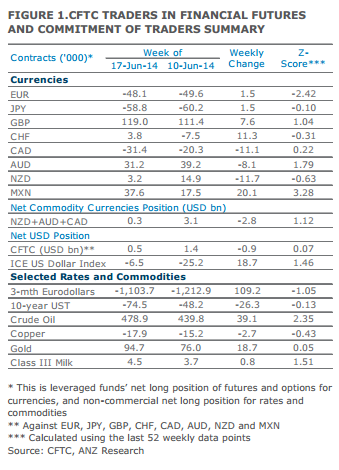

Net EUR position stayed relatively constant for the first time since the start of May when the ECB President hinted of a rate cut that materialised in the 5 June ECB meeting. Net short positions in EUR/USD reduced slightly by 1.5k contracts (worth USD0.3bn) to 48.1k (USD8.2bn). The last time net positioning at this level in mid-2013, EUR/USD was trading closer towards 1.30. For now, EUR/USD is supported above 1.35 and it would require a further increase in short bets to break below that level.

Leveraged funds made a large reduction in net long positions in NZD despite a hawkish 12 June RBNZ Monetary Policy meeting. The positioning change probably reflected the sentiments that NZD/USD was a little elevated . On a relative basis, net long AUD/NZD positions continue to register a new high since late-April 2013 even as leveraged funds reduced their net long positions in AUD.

Net short positions in JPY stayed relatively the same post the 13 June BOJ decision, suggesting that the meeting did little to change sentiments. USD/JPY is not moving as much in line with positioning changes this year compared to the past. Net long positioning in GBP increased by 7.6k contracts to 119k post BoE Governor Carney’s remarks that rate rises ‘could happen sooner than markets currently expect’. Bullish GBP bets should remain elevated.