In short, the ECB delivered:

- Refinancing rate and deposit rate cuts of 10bp

- No new rate cuts in the pipeline

- New targeted funding operation (TLTRO) of 400bn euros plus additional take up

- ABS purchase program preparation

- Prolonged full allotment liquidity provision

Limited room for negativity in rates

The ECB cut its key rates as we expected. The main refinancing rate was brought down by 10bp to 0.15% and the deposit rate to -0.10%. The marginal lending rate was cut by 35bp, making the interest rate corridor symmetrical.

The ECB is the first major central bank experimenting with negative rates. In the press conference, Draghi outlined that the negative rate will apply to reserve holdings in excess of the minimum reserve requirements and certain other deposits held with the Eurosystem – not surprising, since nothing else would have made sense.

Draghi changed the forward guidance to saying that key ECB rates will remain at present levels for an extended period of time. Hence, the ECB will not cut rates further, which is in line with our forecast. However, we were slightly surprised to see ECB outlining so clearly that no further cuts should be expected.

As we expected, the ECB decided to discontinue the sterilization of SMP purchases, which should increase the amount of liquidity in the system by over 160bn euros (though the full amount has not been sterilized every week). ECB will also extend the fixed rate full allotment procedure at least until December 2016.

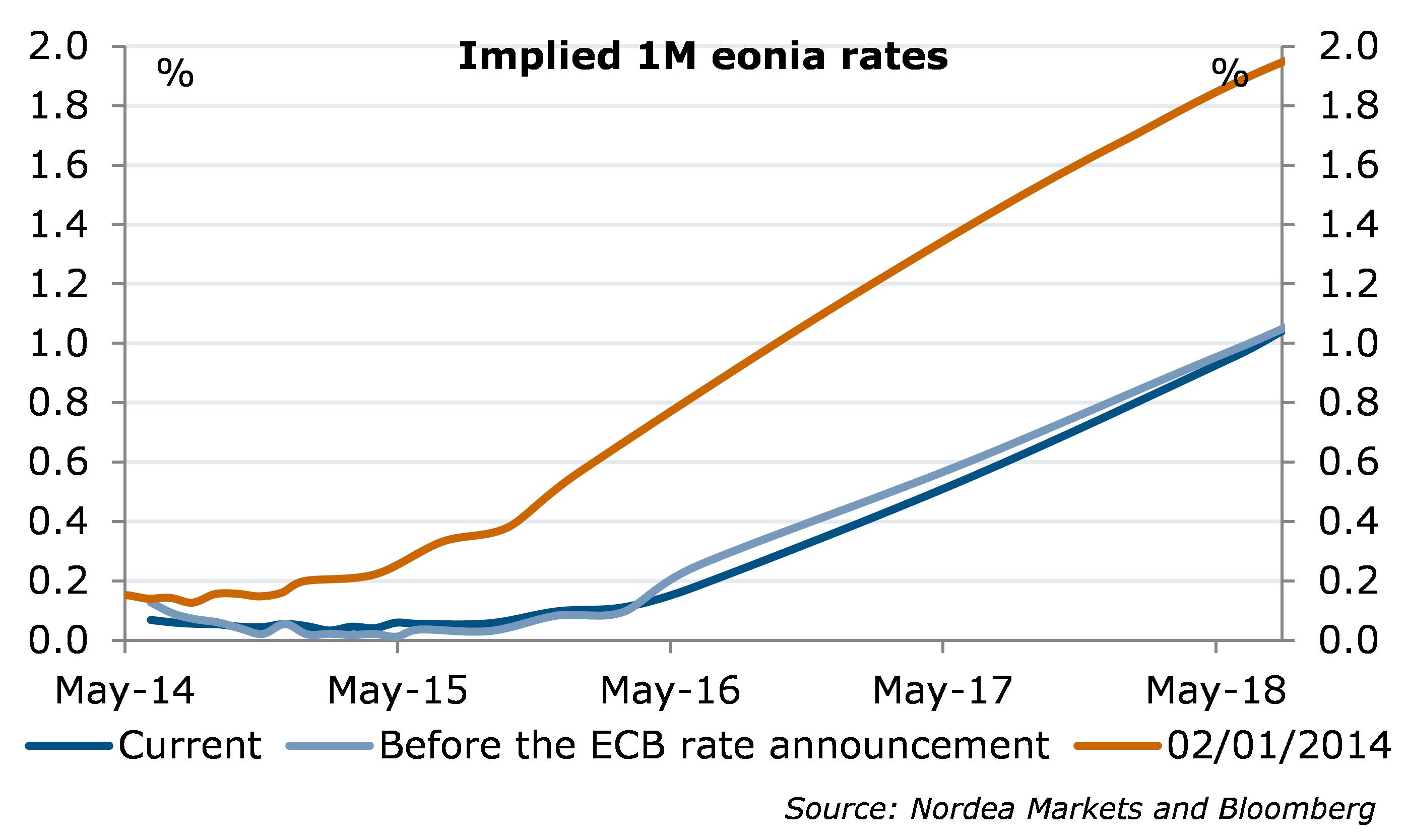

The moves were widely expected, but should decrease the fluctuation in the short end of the curve.

Potentially north of 400bn euros of new measures

ECB will provide a new series of targeted longer-term refinancing operations (TLTROs). Operations will have a maturity of about 4 years until September 2018.

Interest rate on all new TLTROs will be fixed over the life of each operation at the MRO rate at the time of the take up plus a fixed spread of 10bp. In other words, the ECB will offer 4-year fixed-rate loans at rock-bottom rates, which should make it interesting for banks. The fixed-rate can also be seen as a strengthened form of forward guidance, i.e. implying the ECB does not expect to raise rates for a long time.

The initial size can amount to 400bn euros as individual banks can borrow 7 % of their total amount of loans to the Euro-area private sector (corporates and households excluding loans for house purchases). These two successive TLTROs are offered in September and December 2014.

In addition, from March 2015 to June 2016 banks can borrow still more TLTRO’s on a quarterly basis. Here the new take-up can amount to 3 times the net lending to private sector (ex. house purchases) on a specified time.

Operations can be paid back starting 24 months after the start.

The size of operations is likely to stay clearly below the amount seen in the previous unlimited LTRO operations that increased to 1000bn euros. However, the low rate on the funding should support the take up especially in the Euro-area periphery.

Hints of building ABS but not fast enough for summer

ECB will intensify preparations to start outright asset backed securities purchases. The ABS market is however still small and suffering from punitive regulatory treatment. So one should not expect fast changes on this front.

Reason to act: inflation

The lackluster inflation picture is the main reason why the ECB decided to finally act. The ECB cut its inflation forecasts considerably for all the forecast periods (see table below). The forecast for 2016 was brought down to 1.4%.

Support for the recovery but risks still tilted towards the need for more

We took the ECB’s message broadly positive, and see it as another factor supporting a recovery in the Euro-area economy. The package will not be a silver bullet by any means, and risks clearly remain tilted towards the ECB having to provide new measures. Draghi himself said the ECB was not finished, and would do more, if needed.

That said, Draghi also said it would take at least 3-4 quarters to estimate the effects of the TLTROs. As the ECB will want to see the effect of the measures it has taken, it will be reluctant to do much more in the near future. In other words, a broad-based bond purchase programme, or QE will not be in the cards in any case for quite a while.

Steeper curve, narrower spreads, weaker euro

The ECB’s message was good news for risk appetite, bad news for longer core bonds and the euro, at least initially. As the ECB made it rather clear that its benchmark rates had hit bottom, but that they will stay there for a long time, the very short end of the money market curve will stay at depressed levels, but does not really have room to fall further.

On the bond markets, the curve steepened, as longer yields increased on the back of higher inflation expectations, increased hopes that the ECB’s measures would help to kick-start growth and the fact that an easing package was already largely priced in. We see more potential for the curve to steepen and long yields to increase in the near future.

Spanish and Italian Spanish bonds rallied, while intra-Euro-zone spreads narrowed throughout the line. Despite the large moves, spreads continue to have more narrowing potential. After all, the ECB just confirmed that rates will stay at rock-bottom levels for a long time, strengthening the need to find carry.

Regarding FX, Draghi delivered a lot, but what concerns the EUR – deposit rate cut was only symbolic. However, this is the bottom in the deposit rate, and the 10bp negative rate is no game changer. The EURUSD, after taking some stops down here, should find support at around 1.35, and rush back up soon.

Short money market rates with only limited changes

Nordea