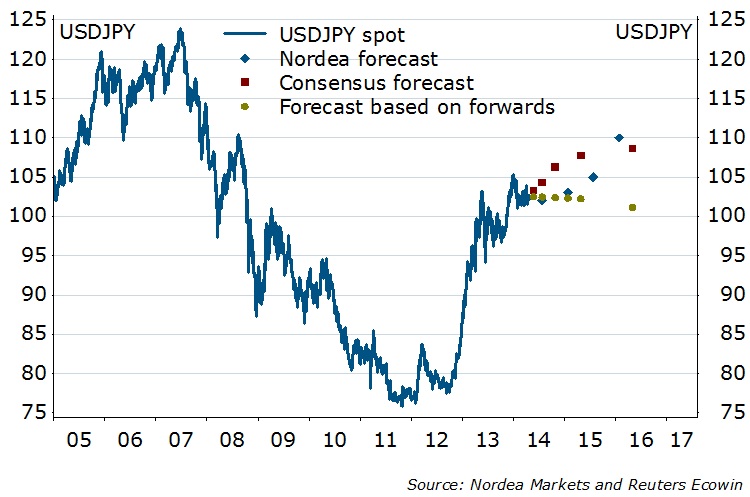

Another BoJ meeting went by with no change to monetary policy. We maintain our long-held stance that no further easing is on the horizon. Japanese equities opened higher and the JPY traded at modest gain vs the USD. Please note that we have recently revised our 3M USDJPY forecast to 102 from 97.

Along with the meeting today the BoJ’s semi-annual outlook report was released. The staff remained optimistic on the long-term outlook but lowered growth projection for fiscal year 2014 from 1.4% to 1.1%, citing a delay in export recovery as the main reason. It acknowledged fluctuations in private consumption due to the consumption tax hike but reiterated that the economy will remain resilient. At this point we believe no monetary easing will be utilised on the ground of the sales tax hike. Our projection on GDP growth is 1.3% for 2014 and 1.0% for 2015.

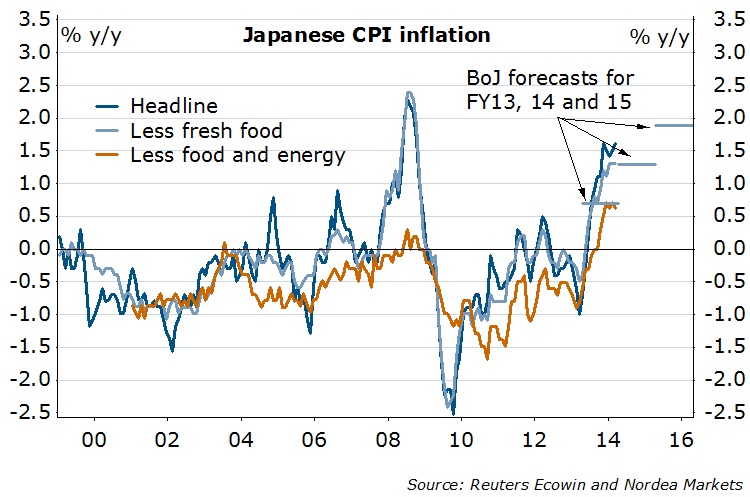

After the CPI data released last Friday, the FY 2013 inflation (less fresh food) became 0.8% and above the BoJ target of 0.7%. The bank remains confident in achieving the 2% price target by around April 2015. Hence, inflation does not give reason to a policy change at this moment.

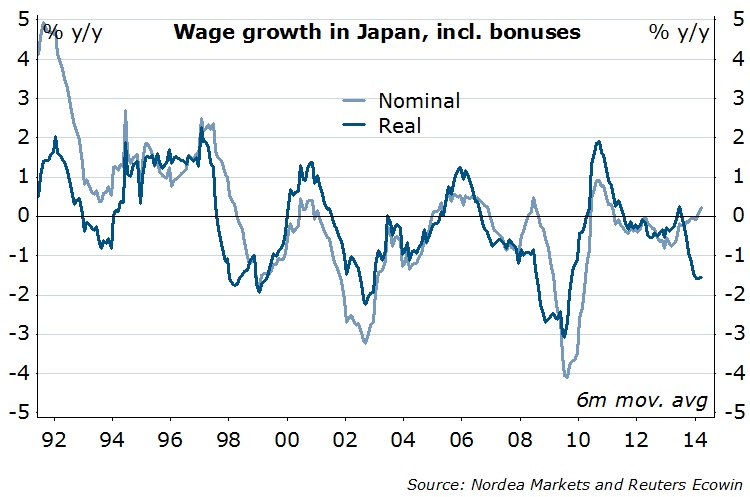

If growth performance disappoints later this year, the lack of deeper structural reform should be blamed and not the sales tax hike. Nominal wages have started rising, thanks to the government’s agreement with large corporations to raise base salary. However, large export-oriented companies only employ 30% of the workforce. As long as the smaller companies, which have not yet benefited from Abenomics, remain reluctant to give higher salary, overall nominal wage will be outpaced by inflation, giving falling real wages and lost consumer confidence.

In this regard, structural reform to improve outlook for smaller companies is a necessary element in Abenomics and cannot be replaced by further monetary easing. This is the only way to create demand-pulled inflation, which is usually associated with positive growth, and not cost-pushed inflation as it is currently in Japan.

Nordea