The National Bank of Hungary (NBH) will continue with its gradual pace of rate cuts at its 28 May MPC meeting, in our view. We forecast a 25bp for the 10th consecutive month, bringing the rate to 4.5%. We maintain our forecast that the NBH will lower rates by 25bp each month until the base rate is reduced to 3.5% by end-September. NBH officials have repeatedly maintained that it will not increase the pace of rate cuts, even though economic conditions support faster cuts. Inflation is well below the target leaving the real rate elevated. While growth has picked up recently, it is still well below capacity. Domestic demand is not likely to exert upward pressure on inflation this year or next. Recent currency appreciation has put further downward pressure on inflation providing more room for cuts.

With inflation low, real rates elevated

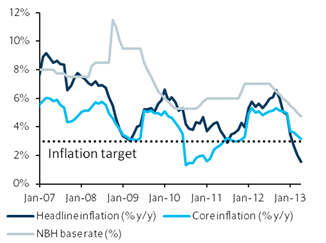

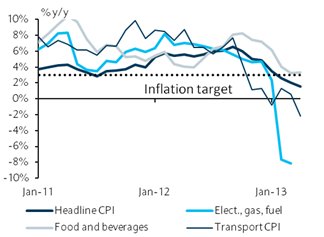

The main support for further cuts comes from very low Inflation. At 1.7% y/y in April, inflation is well below the 3% target, leaving the real rate at an elevated 300bp (Figure 1). There is very little demand driven inflationary pressure in the system. Food inflation at 3.4% y/y is still above the target, but will likely decline in the next months on base effects as the 2013 harvest is expected to be much better than last year’s harvest, which was suffered from drought conditions (Figure 2). Relatively high services inflation at 3.6% y/y in part reflects tax increases (telecom) while excise tax increases have raised the prices of alcohol and tobacco. In contrast, government-mandated reductions of electricity and gas prices have helped bring inflation lower. Further cuts in utilities and energy are scheduled. The NBH predicts inflation will remain below 3% throughout 2013 and 2014 and we see downside risks to the forecasts due to government-mandated utility price cuts.

Growth in a weak recovery stage

While growth picked up in Q1, it remains very low. In Q1, GDP grew by 0.7% q/q but was still down -0.9% y/y. While the string of quarterly declines in growth was broken in Q1, the economy has a long way to go before reaching prerecession levels of output or domestic demand. Thus, inflation will not be threatened by domestic demand pressure, in our view, during 2013 and perhaps beyond. The NBH is implementing policies designed to support growth with subsidized credit to small and medium-sized enterprises through its “Funding for Growth Scheme”.

Currency strength supports further cuts

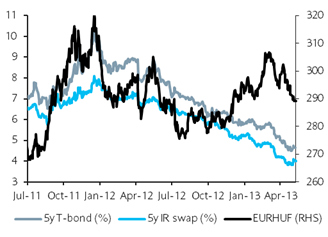

The HUF has appreciated during the past two months by about 6% since the peak versus the EUR. Local currency interest rates have declined (Figure 3). This improvement in the risk environment provides further support for NBH rate cuts. The NBH has all along closely monitored the impact on Hungary’s financial markets of its rate cuts. Declining interest rates and HUF strengthening provides further support for NBH cuts. The NBH is implementing plans to provide longer-term FX swap facilities to banks in an effort to downsize its balance sheet and encourage banks to cut short-term external FX loans.

NBH cuts to continue at the same pace through Q3

We expect the NBH to cut in each of the next five monthly MPC meetings, bringing its rate down to 3.5% by September. The NBH wants to maintain the very slow pace to give markets ample time to absorb the rate cuts. Thus, an increase in the pace of cuts appears unlikely notwithstanding market conditions. Once 3.5% has been reached, cumulative cuts will have halved the base rate and we expect the NBH to pause to assess the impact on financial markets and to assess the long-term inflation trend. We do not rule out additional cuts after a pause, depending on domestic and global macroeconomic developments. But the NBH appears reluctant to push real rates excessively low.

Figure 1: Inflation has declined considerably in Hungary, supporting further cuts

Figure 2: Lower energy prices support the general declines in inflation

Figure 3: Improved risk indicators

Barclays