ECB preview

Assuming an interest rate cut is a given, it’s all about the possibility of other measures to support credit to SME’s in the EU from the ECB today. As I indicated with the short-term EURCHF call idea ( which is even cheaper today, or can be done at a lower strike price) the intriguing scenario to me for EURCHF is one in which the ECB extends new measures that weaken the Euro generally versus perhaps GBP and the USD, but not against the CHF, where systemic risk is likely the more important determinant.

If the ECB provides new accommodation, odds are we look for a challenge of 1.3000 again soon in EURUSD, especially if we close below 1.3200 today. If we see nothing of note from the ECB and merely a 25-bp cut (or a shock no-cut), this would be rather risk negative and could see a more resilient Euro, although one wonders how the single currency can find legs to rally on from here from this angle, as this would tend to aggravate the risk of an immediate return of risks from an irate periphery that needs something to happen soon to bring it relief.

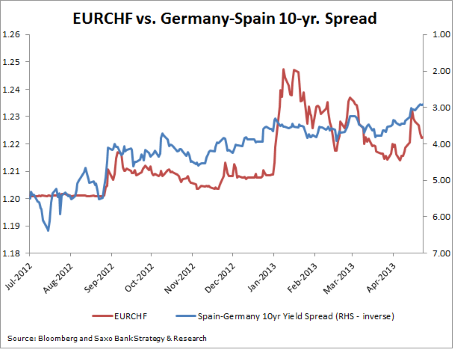

Chart: EURCHF vs. Germany-Spain 10-year yield spread

If the ECB shows more accommodation, it could improve peripheral spread tightening even further and we have seen a general tendency – until the last week’s sell-off – for EURCHF to take its directional lead from this “systemic risk” indicator. Stay tuned…

Looking ahead

An accommodative ECB would also be the interesting test for the general level of risk appetite across markets – does the market fret the Fed’s lack of new accommodation or celebrate new ECB stimulus attempts? The DAX this morning is trying to vote for a celebration of new liquidity – but should German stocks be rallying to new highs as German economic data deteriorates? This is so reminiscent of 2007 in the US when rapidly weakening data saw the Fed finally responding with a larger than expected rate cut in September. Equities jumped for joy and posted a new all-time high in October prior to their subsequent epic collapse.

Don’t forget we have some interesting data out of the US today, including another weekly jobless claims figure and the March Trade Balance data. The key data to put the kibosh on this critical week comes tomorrow with the US employment report and ISM non-manufacturing. The latter is critical for indicating how close we are to falling into a new recession in the US.

SAXO BANK