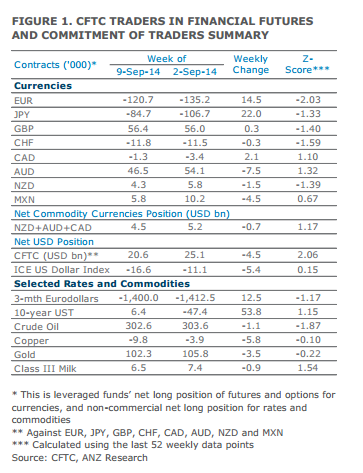

Leveraged funds decreased their USD exposure for the first time in eight weeks. This was in spite of the DXY index rising 1.5% in the week ending 9 September. We suspect the reduction in positions were profit taking as opposed to a change in view about the direction of the USD.

Net long USD positions decreased by USD4.5bn to USD20.6bn. The decline in USD positioning was primarily caused by an unwinding in short positions in JPY and EUR. We are likely to see net long USD positions rebuild ahead of this week’s FOMC meeting, where markets are anticipating a change in the Fed’s forward guidance language.

Net short positioning in JPY declined by USD2.7bn to USD10.0bn. This reduction from historically elevated levels likely reflected profit taking after the recent depreciation in the JPY. But with the JPY coming under further depreciation pressure following the CFTC cut-off date, we suspect leveraged funds have rebuilt their net short positions.

Net short positioning in EUR also declined by USD2.7bn to USD19.5bn, even as EUR/USD fell from 1.31 to 1.29. This unwinding of short positions likely reflected leveraged funds taking profit following the 4 September ECB meeting.

Despite the intensifying focus on the upcoming Scottish referendum and the sharp decline in sterling, we saw little change in overall net positioning in GBP. The outcome of the referendum looks like a coin toss at this stage, and market positioning will likely shift sharply depending on the results of the vote on 18 September.

Net long positioning in the AUD and NZD declined by USD0.7bn and 0.1bn respectively. Both currencies fell further after the CFTC cut-off date, indicating a further unwinding of net long positions. Between the antipodean currencies, there is more potential downside from a positioning purge in AUD.