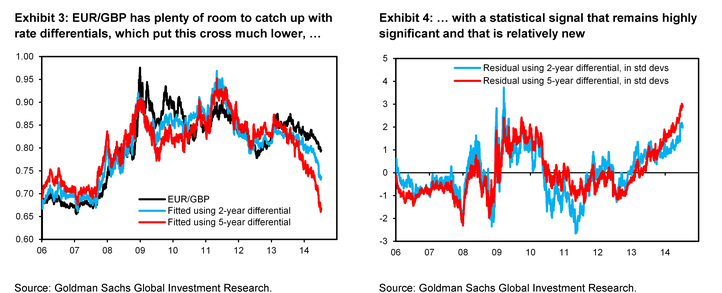

Our strongest conviction in recent months has been that EUR/GBP should continue to move lower. Exhibit 3 shows our model for this cross, where the blue line shows the fitted value using the 2-year differential (in addition to controlling for Euro periphery 10-year yield spreads over Bunds, the VIX as a proxy for global risk appetite and oil prices) and the red line shows model output using the 5-year differential. What stands out is that EUR/GBP has lagged the sharp move in rate differentials, so that – even though front end rates in the UK have moved quickly to reflect the change in rhetoric from the Bank of England – there is plenty of room for the move lower in EUR/GBP to extend further…

…While our GBP and CNY views are medium-term views, we think this week’s BoC meeting could present a short-term opportunity. This is because the sharp rise in Canada’s inflation has many in the market expecting the BoC to turn more hawkish. To be sure, we expect the MPR to revise up the inflation forecasts for both headline and core CPI, but we are firmly convinced that Governor Poloz will maintain his dovish focus given that core inflation remains in the lower half of the target band and that adverse fallout from a policy switch could be considerable. We see this as actionable because speculative positioning has, according to the CFTC’s CoT report, gone flat in recent weeks, as the market has lost patience with the $/CAD higher trade. We see this week as an opportunity to position for $/CAD higher, as a continued dovish tone from the BoC could wrong-foot the market.