The following are the key points in ANZ’s analysis for the latest speculative positioning report (positioning data is for the week ending 24 June).

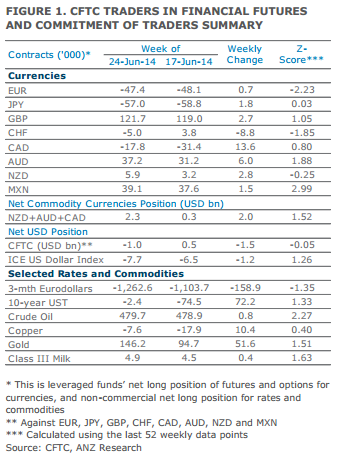

USD positioning among leveraged funds stayed relatively unchanged as net positioning in the major currency pairs (except CHF) had muted changes. Leveraged accounts turned net short USD to USD1bn from net long USD0.5bn the prior week, possibly post FOMC meeting with Chairman Yellen pledging continued monetary accommodation.

Net EUR position stayed relatively constant for the second week in a row. Net short positions in EUR/USD reduced slightly by 0.7k contracts (worth USD0.1bn) to 47.4k (USD8.1bn).

Net long positioning in GBP stayed elevated, increasing by 2.7k contracts to 121.7k as the market continued to price in a hawkish BOE.

On a relative basis, net long AUD/NZD positions continued to register a new high since late April 2013 even as leveraged funds restocked their net long positions in NZD as net long positions in AUD increased by more in comparison.

CHF positioning turned net short again after a one week pause. Net CHF positioning turned net short 5.0k from net long 3.8k the prior week.