The outlook for oil prices have moved on to investors driven by potential supply disruptions as tensions rise in Middle East. Brent crude oil, the global benchmark, now stands at $114/bbl after it rose over 8% since late May. At $114/bbl this is 7.8% higher than the 2014 average of $107.29/bbl while the front-end of the Brent crude oil futures curve has steepened notably over the past month.

Overall, while demand from the mature countries, such as the US, have steadily declined over the past few years, recent tensions in Iraq have raise concerns about tighter global supply. Recall, Iraq production averages about 11% of OPEC’s total daily production given it reserve potential was expected to pick up production over the coming years.

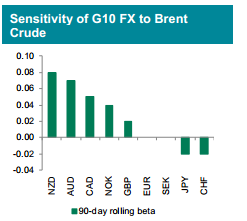

With markets now focused on the fluid situation in Iraq, we seek to quantify the risks of a spike in oil prices and the impact on G10 currencies. For this exercise, we looked at the rolling 3-month betas (first difference of the log value) of the G10 currencies and Brent crude oil. The beta measures the percentage change in the currency for a ten percent change in Brent.

The biggest beneficiaries of a rise in Brent are NZD, AUD, CAD and NOK, according to our analysis.

While a positive terms of trade shift is likely at play, monetary policy expectations are also important here. Indeed, given the inflationary impulse a sharp in oil prices it is no surprise that GBP, AUD and CAD have benefitted from a rise in oil.

At the other end of the analysis is JPY and CHF and to a lesser degree EUR and SEK. Most of these countries are net oil importers so a rise in oil prices is associated with currency weakness – especially in the case of JPY.

The bottom line is that given the generally benign inflationary environment a surge in oil prices could help amplify the divergence in monetary policy and help boost the currencies that 1) might normalize monetary policy sooner that expected and/or 2) benefit from a rise in terms of trade.

Credit Agricole