- We expect very dovish signals from the ECB at this week’s monetary policy meeting, but no change in key rates.

- Risks are clearly skewed towards another rate cut and the door is likely to be left wide open to all non-conventional measures including a negative deposit rate, LTROs or possibly even QE.

- We could easily see the ECB announcing new liquidity measures to ease concerns around the turn of the year.

We expect no fresh rate cuts at this week’s ECB meeting

We expect the ECB to keep rates unchanged at this week’s meeting.

The next step on rates could be a further refi rate cut to 10 bp or 15 bp, but the effect is likely to be fairly limited unless the deposit rate is cut as well, and we believe it will take a greater sense of urgency to move the ECB down that road.

Inflation ticked up again in November to 0.9% (from 0.7% in October) and core inflation to 1.0% (from 0.8%), which reduced the pressure on the ECB to act again this soon.

Incoming data since the November meeting confirmed that the recovery is weak with lower-than-expected GDP and credit figures, hence the tone is likely to be very dovish and the door for more action will be kept wide open, be it negative deposit rates or LTROs or perhaps even QE. There is simply no reason for the ECB to deny any possibilities.

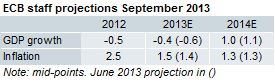

New staff projections to show low inflation for a while

New staff projections are likely to confirm that inflation will remain very low in both 2014 and 2015.

We expect the inflation projection for 2014 to be revised down 0.1-0.2% point, while the new 2015 projection is likely to be around 1.5%.

{kind=link}

The near-term inflation readings will be crucial for the ECB. The recent very low readings have affected medium-term inflation expectations implied by the markets, say 5Y5Y forwards from inflation swaps, which dropped after the surprise October inflation print.

The very low inflation readings also highlighted the risk of outright deflation.

New liquidity measures possible

We could easily see the ECB announcing new liquidity measures to ease concerns around the turn of the year.

The Asset Quality Review will be based on bank balance sheets as of 31 December and could, together with the recent significant drop in excess liquidity, lead to tighter liquidity conditions around the turn of the year.

The ECB could (temporarily) suspend SMP sterilisation or add new liquidity operations to loosen liquidity conditions around the turn of the year. We have already seen EONIA moving slightly higher well ahead of the month-end and a failure to fully sterilise SMP holdings. The ECB might suspect that fully sterilising SMP holdings could be difficult for the rest of the year anyway.

Nordea