Markets may shrug off the downgrade of France by S&P for now as they have become accustomed to worse than small downgrades from AA+ to AA. According to S&P, “… French government macro-economic reforms will not substantially raise the country’s medium-term growth prospects.” Here we follow up on that with calculations about the path public debt (relative to GDP) could take from here to 2018.

A “sustainable debt level” – what does it mean?

Nobody knows exactly what a sustainable level of public debt is. While for some countries, 70% of GDP may be enough to frighten investors, for others more that 100% may be bearable, at least for a while. But debt cannot rise forever, that’s for sure. The IMF defines it like that:

“In general terms, public debt can be regarded as sustainable when the primary balance needed to at least stabilize debt under both the baseline and realistic shock scenarios is economically and politically feasible, such that the level of debt is consistent with an acceptably low rollover risk and with preserving potential growth at a satisfactory level.”

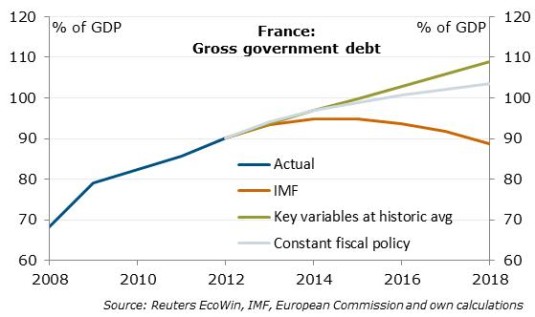

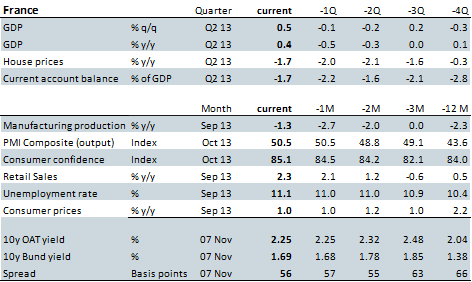

So it’s about the fiscal balance and growth, and there should be a safety margin because unforeseen shocks can happen. Public debt in France amounted to 93.5% of GDP in Q2 2013, up from 64.2% in Q4 2007. We did a sustainability analysis that tries to answer the following questions:

- What’s the debt level in 2018 if the determining factors – nominal GDP growth, interest rates, fiscal balance – remain at their average value between 2003 and 2012 (the green line in the chart)? Over that period, average nominal GDP growth in France was 2.8%, real growth just 1.1%.

- Where does the debt level end in an IMF scenario assuming an acceleration of nominal growth to 3¼% p.a. between 2014 and 2018 (the brown line)? The IMF also assumes that public borrowing falls below 3% in 2015. This is optimistic and not our or the European Commissions’ view.

- What happens to the debt level in a scenario where all the variablse follow IMF expectations except for the stance of fiscal policy that remains at is was in 2012 (the light blue line). That means, the structural primary deficit remains at 1.2% through to 2018.

One doesn’t have to be a doomsayer to consider a debt ratio of more than 100% possible

With no improvement in growth and fiscal balances, debt rises to around 110% of GDP in 2018. With IMF growth assumptions and no additional fiscal effort compared to 2012, debt to GDP still rises to 104%. In the IMF scenario, the debt ratio peaks in 2014/15 (at 95%) and falls to 89% by 2018. So under the IMF assumptions, the debt ratio goes down, but not a lot.

We cannot answer how markets would react to GDP rising above 100%. That depends on many things, also on how other countries are doing. And to be fair, France has implemented a restrictive fiscal policy and the primary balance probably improves again this year. But given 1) that the debt level is rather high, 2) that the process of implementing growth-enhancing reforms is slow and 3) that negative shocks can happen, we are still worried. Not so much about fiscal policy, but about the lack of growth.

Nordea