• Key policy rate unchanged, at 1.5%; path lowered by 0.45bp at the most

• Lower pressure in the Norwegian economy, along with lower cost and price pressures ahead

• 50% chance of interest rate cut in Q3 this year; clear downside risks

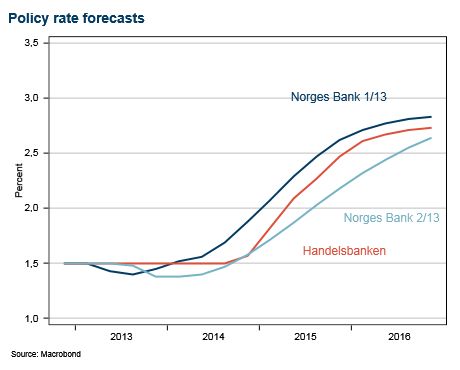

Norges Bank keeps policy rate unchanged at 1.5% and lowers key policy rate path by 0.45bp at the most

As we expected, Norges Bank decided to keep the key policy rate unchanged at 1.5% and lower the path for the key policy rate by 45 basis points (bp) at the most. The new path for the key policy rate implies a 50% likelihood of an interest rate cut in September this year. As with the key policy rate path from March, there may be more a technical possibility than a real possibility of a cut, but it highlights the downside risks to the Norwegian economy at the moment. The downward adjustment of the interest rate path was due to the factors we had foreseen. The lowering was somewhat larger than we had anticipated, but we had pointed to a downward risk.

Lower pressure in the Norwegian economy along with lower price pressures ahead pull down

The lowering of the interest rate path was due mostly to to lower capacity utilisation in the Norwegian economy and lower cost and price pressures ahead. The fact that Norwegian banks are increasing interest rates also pulls the interest rate path down. Economic growth prospects among Norway’s trading partners also contributed. Somewhat higher than expected inflation in recent months, the weaker than expected krone and somewhat lower money marked spreads contributed to pulling the interest rate path up.

Inflation and bank margins represent a clear downside risk to the key policy rate this autumn

In its new monetary policy report, Norges Bank decided not to cut the interest rate despite cost and price pressures in the Norwegian economy currently being very low. In the new report, Norges Bank expects inflation to reach only 1 3/4% by the end of 2016. The current weak inflation poses a clear downside risk to the interest rate path. Should inflation turn weaker than Norges Bank currently expects, Norges Bank would have to cut the interest rate in September. The fact that banks are tightening credit conditions is also a downside risk to the interest rate this autumn, the way we see it. Should Norges Bank advise banks to hold a countercyclical capital buffer on top of already-stricter new capital requirements, banks could raise interest rates by more than Norges Bank currently foresees. In that case, Norges Bank might also be forced to cut the interest rate to prevent economic activity in Norway easing by more than currently foreseen.

Handelsbanken