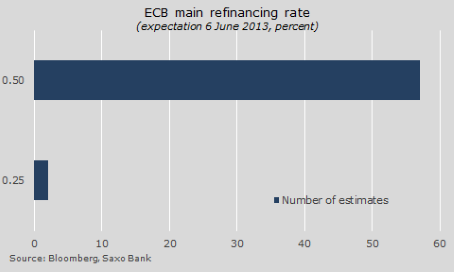

Bottom line: Since the European Central Bank cut its main refinancing rate by 25 basis points to 0.50 percent on 2 May data has generally been better than expected, which limits the need for further action at this point. Hence, we do not expect anything major from the ECB today.

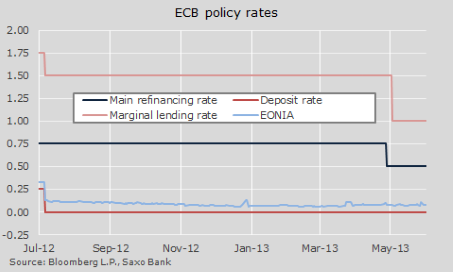

Details: The ECB’s move to cut rates at its meeting on 2 May where the main refinancing rate was lowered to 0.50 percent and the rate corridor was narrowed to 50 basis points (marginal lending rate: one percent, deposit rate: 0 percent) came just as data started to improve and seemed like an act of desperation with the ECB wanting to show that it is doing ‘something’. We do not expect that rate cut to have a material impact on the real economy and we believe that the ECB should instead have focused on a credit-enhancing programme for small and medium-sized companies – though this may come at a subsequent ECB meeting.

Furthermore, another cut to the main refinancing rate would likely prompt the governing council to also slash its deposit rate from 0 percent. But while ECB president Mario Draghi said recently that he was open to the idea of negative deposit rates, we believe that there is still widespread disagreement within the council. Bank of France governor Christian Noyer said in late May that “this is technically very delicate. I’m personally not convinced there’s an interest in doing that” joining the Bundesbank’s Jens Weidmann.

Every quarter, the staff of either the ECB or the Eurosystem give their updated macroeconomic projections for GDP and inflation. We expect today’s report (from the Eurosystem officials) to show a slight downward revision of 2013 GDP growth from the currently-expected contraction of 0.5 percent. Meanwhile, 2014 growth could well be revised up a tad from its present one percent. Inflation, currently seen at 1.6 percent this year and 1.3 percent in 2014, could be lowered as Brent oil prices have dropped more than 10 percent since their February peak.

SAXO BANK