Tight fiscal policy by way of spending cuts and tax increases is one of the key reasons why the Euro area struggles to get out of recession. Expectations for a return to growth next year are usually based on the premise 1) that the world economy provides support for exports and 2) that the worst part of the fiscal adjustment is over. Recently, the European Commission accorded more time to several countries to lower deficits below three per cent of GDP. So, will fiscal policy provide a boost to growth or will it at least be less of a drag?

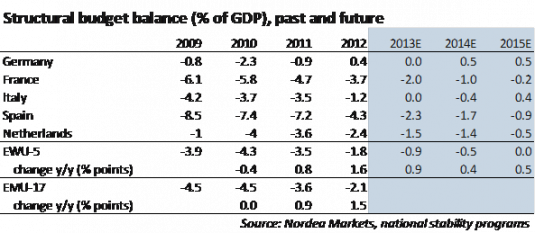

It will be less of a drag this year compared to last and also next year compared to this when looking at plans for the so-called structural budget positions that were published in the latest round of Stability Programmes in April/May. In calculating structural surpluses/deficits both the influence of the business cycle on public finances and of certain one-off measures are excluded. 2012 was by far the toughest year in terms of deficit reduction (see table below). No wonder that domestic demand fell in each single quarter of last year. With a planned tightening of almost one percentage point this year, the impact on growth will still be significant. Applying for simplicity’s sake a fiscal multiplier of one, that means that tight fiscal policy “costs” almost one per cent of GDP this year, or € 85 bn. If reality follows the plan, policy will be less (but still) restrictive in both 2014 and 2015.

However, reality often differs from plans, also when it comes to fiscal policy. In the past few years, some governments did not tighten fiscal policy as much as was originally planned. In spring 2011, for example, France aimed for a structural deficit of not bigger than 2.9% in 2012; the actual outcome was -3.7%. Spain aimed for -3.5% and arrived at -4.3%. On the other hand, Germany and Italy – under the Monti government – improved budget positions much more than planned. So history does not tell us that we should always and everywhere expect higher deficits/lower surpluses compared to what politicians “promise”. Going forward however, given the anti-austerity climate in Europe, it seems reasonable to expect some slippage of fiscal policy. If so, the improvement in structural budget positions could turn out to be a bit weaker than shown in the table. That can be good for growth if at the same time confidence doesn’t suffer.

What is unlikely to happen, though, is a major fiscal boost from Germany, the only major Euro-area economy with a structural budget surplus in 2012. The election race is open for now. But even if Social Democrats win on 22 September, a gradual and limited policy change is much more likely than a u-turn towards loose fiscal policy.

Nordea