• After a pretty hectic ECB meeting a month ago, we expect a somewhat more calm sentiment around this week’s event, but rates may still fall.

• We expect no change in rates and nothing new on the ABS programme this time around.

• Draghi is likely to strike a dovish tone to support sentiment and confidence, probably stressing recent key figure improvements and keeping the option of negative rates on the table.

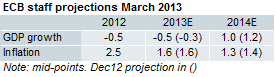

• The growth projection is likely to show a slightly downward revision, but we expect the key 2014 inflation projection to be unchanged at 1.3%.

The ECB is widely expected to keep rates unchanged at this week’s meeting. Rates were cut in May, sentiment remains fairly solid and key figures have improved. The sense of urgency that had built up ahead of last month’s meeting is replaced by a sense of calm this time.

The ABS programme remains top priority, but there is not much more the ECB can do. It has already expressed its willingness to provide funding and its unwillingness to take on the credit risk. The EU Summit 27-28 June may be the next important step towards an ABS programme, since government involvement to help the European Investment Bank lift the credit risk involved in a larger-scale ABS programme seems necessary.

Market expectations should not be particularly high either. In fact, an unchanged message from Mr Draghi would likely suffice to put some downward pressure on rates after the upward move we have seen since the May meeting.

Negative interest rates and exceeding expectations

We believe that the ECB president has become more focussed on meeting or even exceeding expectations. There is not much more the ECB can do in the current situation, but at least the ECB president can give verbal support to sentiment and thereby help support confidence, which remains a crucial element of a recovery. We therefore expect Draghi to strike a fairly dovish tone and keeping the option of negative interest rates on the table. He may also take notice of the recent improvement in key figures. The PMIs and the Ifo have improved, inflation rebounded as Draghi indicated at the May meeting, and industrial production increased sharply.

Slight downward revision of projections

The new staff projections are likely to show a slight downward revision from the already bearish March projection. GDP growth for this year is likely to be revised slightly lower from the March projection of -0.5% to something closer to our new -0.8% forecast, which will also take down 2014 slightly. The expected modest recovery in the second half of this year is likely to remain in place.

The most important projection is for inflation next year. We find it difficult to see the ECB project a much lower inflation rate without taking new action – saying that 1.3% inflation is close to but below 2% is already a stretch. The projection for inflation is likely to be revised down for this year due to the drop in oil prices. However, since the ECB uses market pricing in its projection, energy prices will lift inflation slightly for next year compared to the March projections, which is likely to counter the effect of weaker growth, leaving this projection roughly unchanged.

The ECB remains data dependent

All in all, our take on this week’s meeting is long words, short action. Draghi is likely to be dovish to support sentiment and will most likely continue the talk about negative interest rates, but more action is pending incoming data. Key figures must improve gradually from here for the ECB’s projected recovery to materialise. If not, we believe the barrier to more action is fairly low.

Nordea