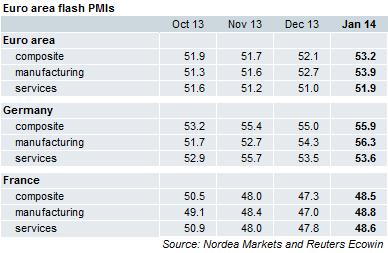

The composite reading of 53.2 is compatible with GDP growth of around 0.3% q/q for the Euro area. Of course that has to be confirmed by hard data which are still lacking for Q1. In manufacturing, the employment component rose above 50 for the first time since January 2012. New orders and export orders are quite solidly in the 55 points area.

Germany delivered strong readings. The new orders component in the manufacturing sector approaches the 60 level. There are no sings that the “strong euro” does a lot of harm to exporters. There are no signs either, however, that employment growth will accelerate significantly.

For France, it was time to catch up at least a bit and so it happened, but only in the service sector. Readings between 48 and 49 still indicate weak growth at best. GDP growth in the winter half-year could be quite volatile as the VAT hike (for the standard and the intermediate rate) in January might have brought consumption forward from Q1 to Q4 of last year. For GDP, we pencilled in 0.3% q/q for Q4 and 0.1 for Q1 for now.

For the ECB, these numbers will confirm that the recovery goes on and that it might gain some strength. If the ECB decides “to do more”, it will not be because growth disappoints but for money market considerations and/or because inflation is still so low.

Nordea