The 4% stronger USD this year, impact on inflation – is it enough to worry Fed? Maybe not yet. But… what else?

It is 20 years next year since the US Treasury Secretary R. Rubin famously announced that “strong dollar is in our national interest”.

Is it?

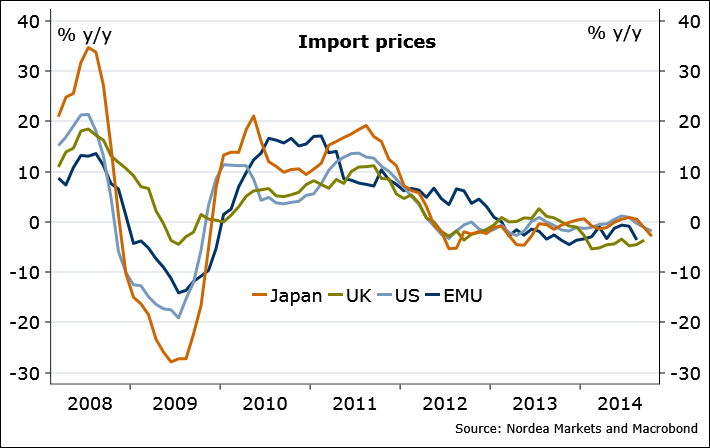

Firstly, inflation. The US is being dragged in global disinflationary trends (Figure 1). Market-based US inflation expectations have moved in lockstep with the USD this year – stronger USD, lower breakeven inflation rate. I haven’t seen Fed’s estimates of exchange rate impact on inflation recently, but ECB and BoE have provided theirs: 10% effective appreciation brings inflation down by 0.5%pt and 1%pt, respectively. The USD NEER is more than 4% up this year alone, should be at least 20bps downside effect on inflation. Huge? Not yet for Fed to worry, but just wait… (EMU inflation figures – this week’s highlight).

Figure 1. Stronger currency, anyone?

Apart from the topical effects on inflation, there is also impact on the trade balance from the value of the USD – cheaper currency should help net exports. Ceteris paribus. In theory. But with the current degree of globalization, and with the US being a rather closed economy, I doubt there is a reason to hope that a weaker USD could drive US growth – not in my lifetime.

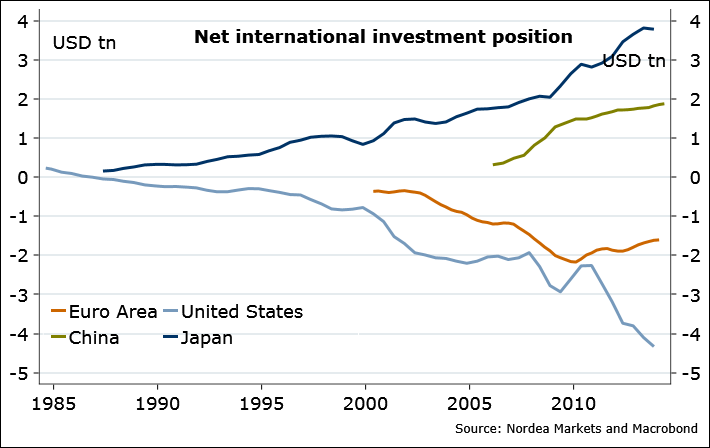

Thirdly, and most interestingly, valuation effects. That’s linked to the trade balance, the major component of the US current account. We know that US has been running current account deficits over the past 30 years. The current account flow is accumulated to what is called “international investment position”. As a result, the US has become the largest debtor toward the rest of the world, currently owing close to USD 4.5 trillion (net)!

Figure 2. World’s largest debtor…

Seems large? Just wait. The international investment position, in Figure 2 above, accounts for valuation changes (in contrast to the current account). So, there has been a gap created (Figure 3) – the US has massively benefited from valuation effects over those 3 decades. And the USD is part of the story.

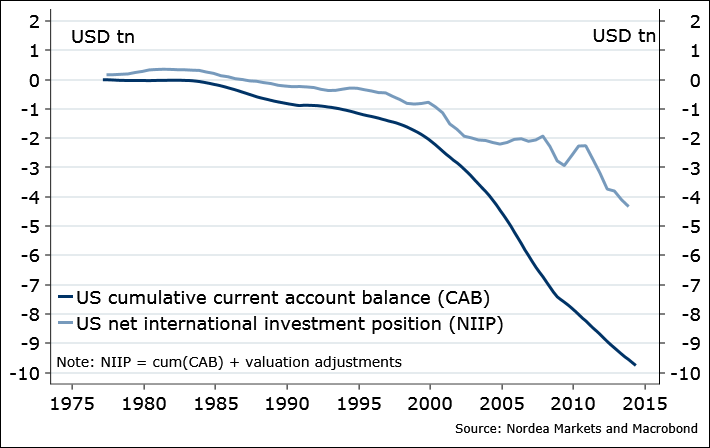

Figure 3. If not valuation effects, US would own close to USD 10 trillion to foreigners!

Looking at US international assets and liabilities separately, the US external assets are nearly exclusively in USD, and mostly in government sovereign debt. It does make sense for the US inflating the USD. According to some estimates, a 10% depreciation of the USD represents a 4 to 6% transfer of the US GDP from the rest of the world to the US!

Figure 4. Source of US net foreign asset gap is within portfolio investments, in particular debt…

![]()

Figure. 5. …in particular, US Treasury bonds

The US foreign asset side is more interesting. The US primarily invests in foreign equity and other “risky” stuff, of which most (around 70%) of is in foreign currencies.

Figure 6. Number 1 currency exposure – asset side

So yes, in fact it is very much in the US’ interests that foreign currencies appreciate, and in particular the European assets appreciate and the EUR gets stronger. According to one prominent study, “the magnitude of the gains depends on which currency the dollar moves against, with a depreciation against European currencies generating a more substantial effect than an equal depreciation against Asian currencies.” No wonder the pressure from IMF, Fed and American think-tanks for ECB to do more QE…

Oh well.

Nordea