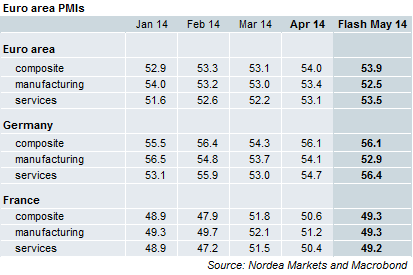

As we had expected the manufacturing PMI for the Euro area slightly declined while the service component went up. New orders and export orders in manufacturing don’t give reason to worry that manufacturing production will decline over the next months.

German numbers were okay with the composite PMI unchanged. The service PMI rose to its highest reading since mid-2011, highlighting the strength of domestic demand. The new orders component in manufacturing declined but still looks healthy. While the economy is on track, strong Q1 GDP growth of 0.8% q/q was due to exceptional circumstances and will not happen again in Q2 or Q3.

France – the economy that rarely fails to disappoint

French PMIs are down below 50 again. Forward looking components like new orders and new export orders are below 49. One should not take took much out of these volatile numbers but the message could not be clearer: The French economy stagnated in Q1 and it does not look much better for Q2, although the neighbour and biggest trading partner east of the Rhine expands at a healthy pace. France needs so much more to get back to healthy growth than what the ECB can deliver. No surprise that many German policy makers may agree to more conventional stimulus from the ECB but don’t want QE which would very likely reduce the incentives for the French government to “do its homework”.

Nordea