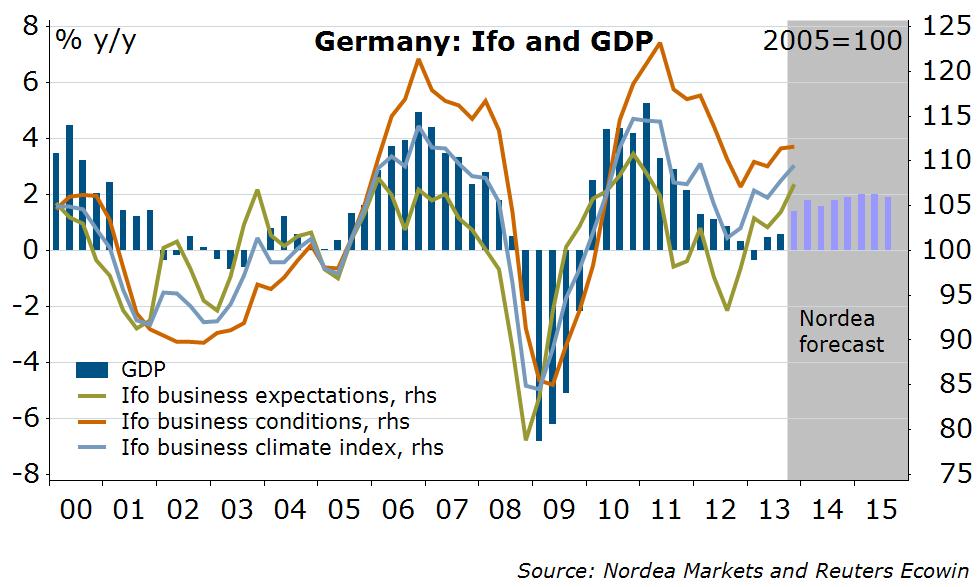

German companies are looking optimistically into 2014. The Ifo business climate virtually stagnated in December, but expectations were raised. All three main ifo components (business climate, current situation and expectations) are well above their long-term average. We expect German GDP to grow by 1.6% next year, driven by domestic demand and well ahead of the Euro area as a whole. The driving forces are several of the reforms undertaken by former governments, low interest rates, rising disposable income, a broadly neutral fiscal stance and – if we take out important parts of the Euro area – a supportive environment for exports.

Sentiment indicators like Ifo, ZEW and PMIs are pointing towards an upside risk for our GDP forecast of 0.3% q/q in Q4. However, hard data are pointing towards a weak start to Q4, as retail sales as well as industrial production and construction output fell over the month in October. Therefore 0.3% q/q is still the forecast we feel most comfortable with.

If German GDP surprises in the upside, that wouldn’t necessarily mean stronger momentum in the Euro, as other things are not equal. Once again, France gives reasons to worry. Given that the PMI composite output index fell to 47 in December, our forecast of a ¼% q/q GDP increase in Q4 could be too optimistic. We are not the most optimistic forecasters on France, however: Based on its own business surveys, Banque de France recently increased its growth expectation to 0.5% q/q (from 0.4%). We will see.

Nordea