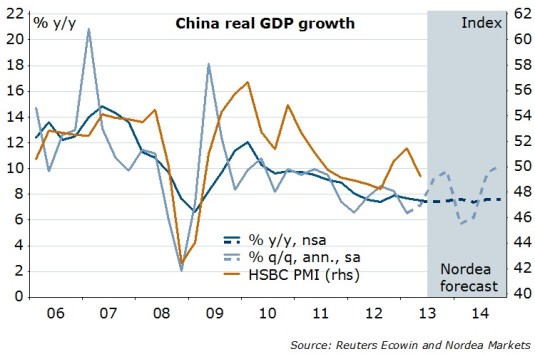

The Chinese economy lost speed further in Q2 and grew by a mere 7.5% y/y, in line with market consensus and slightly above our forecast of 7.4%. The accumulated growth rate for the first half of 2013 turned out to be 7.6% y/y.

The National Bureau of Statistics reported that investment contributed 4.1% points to the H1 (not Q2) GDP growth, consumption 3.4% points and net exports 0.1% points. This is a clear indication that investment remains the largest growth engine, but consumption is gradually gaining importance.

The slowdown is due to a mix of cyclical and structural reasons. Cyclically, the weak global and domestic economy caused exports and industrial production to stall. In June, exports fell by 3.1% y/y and industrial production only grew by 8.9%.

Structurally, China has reached the point, where fundamental reforms are necessary to tackle the country rising problems with overcapacity in the industrial sector and credit risk in the financial system. Beijing has changed its attitude rather drastic and has held hands off both monetary and fiscal policies. Premier Li Keqiang has explicitly turned down the option of another large-scaled investment package.

Towards the end of this year, we expect a stabilisation in the Chinese economy. The cyclical slowdown is likely to be corrected by an improvement in the US economy and a stabilisation in the Eurozone. The policy makers will remain determined on implementing structural reforms at the expense of short-term growth, so unless the economy deteriorates more than what is tolerable for the authorities, monetary and fiscal policies will be kept at status quo, i.e. no rate cut in 2013. We also believe that upside potentials in the CNY is limited, as the authorities would want to keep the currency as a potential tool to offset some of the lost competitiveness earlier this year.

A recent statement by the finance minister, Lou Jiwei, has confused the markets about China’s official growth target. We want to highlight that no indication of a downward revision of the target has come from the premier or the State Council. Furthermore, a target revision requires an approval in the parliament (the National People’s Congress) which has not occurred either. Thus, we still expect that the official growth target this year is 7.5%.

Nordea