If you wish to receive Societe Generale FX Daily pdf research report (and many other) on a daily basis, subscribe now or request a free 5-day trial.

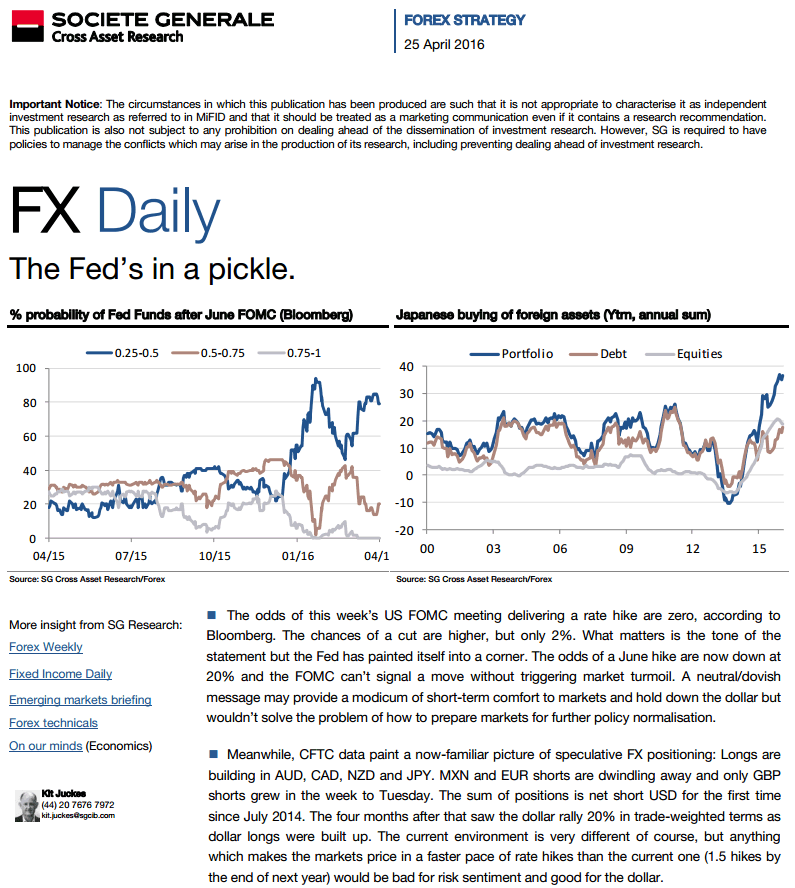

■ The odds of this week’s US FOMC meeting delivering a rate hike are zero, according to Bloomberg. The chances of a cut are higher, but only 2%. What matters is the tone of the statement but the Fed has painted itself into a corner. The odds of a June hike are now down at 20% and the FOMC can’t signal a move without triggering market turmoil. A neutral/dovish message may provide a modicum of short-term comfort to markets and hold down the dollar but wouldn’t solve the problem of how to prepare markets for further policy normalisation.

■ Meanwhile, CFTC data paint a now-familiar picture of speculative FX positioning: Longs are building in AUD, CAD, NZD and JPY. MXN and EUR shorts are dwindling away and only GBP shorts grew in the week to Tuesday. The sum of positions is net short USD for the first time since July 2014. The four months after that saw the dollar rally 20% in trade-weighted terms as dollar longs were built up. The current environment is very different of course, but anything which makes the markets price in a faster pace of rate hikes than the current one (1.5 hikes by the end of next year) would be bad for risk sentiment and good for the dollar.

■ The merest whisper of further BOJ action at Thursday’s meeting was enough to scare some of the yen longs (and revive interest in the Nikkei). Most likely is that the BOJ will borrow from the ECB playbook and lower the cost of some loans to banks, to help offset the effects of January’s move. That won’t have much significance, and it’s not surprising that the yen is a bit stronger this morning. However, I do think the CFTC data accurately reflect short-term market sentiment and as Japanese demand for foreign assets remains incredibly strong, we look for further yen weakness in the few weeks.

■ European news doesn’t look likely to be the driver of the Euro. Treasuries/Bunds are in a range, like the currency. Money supply data are due Wednesday and should be reasonably encouraging, while Q1 GDP data are due on Friday, showing annual growth slowing to 1.5% from 1.6% which is neither here nor there. The chances of a re-run of the Spanish elections in June seem high but that’s not really a new development either.

■ Bookmakers reacted to the intervention of President Obama in the UK’s EU referendum debate by lengthening the odds of a ‘leave’ vote. Politically-inspired sterling shorts are being squeezed as a result, but the news that a major High Street retailer is in danger of administration is a reminder of headwinds facing the economy. Q1 GDP is likely to come in a 0.4% q/q, steady at 2.1% y/.y but definitely on a slowing trajectory. The scale of sterling short-covering is best seen in EUR/GBP, which looks overdone under 0.78. We’ll stick with short GBP/NOK as the best way of reflecting twin views about oil (cautiously positive) and the UK economy (gloomy).

■ Other ways to express views: Short EUR/RUB remains attractive. Jason still like shorts in SGD/INR. There’s about more to take out of shorts in USD/CAD and AUD/NZD longs are still performing, while we still like shorts in CHF/SEK. But the time is coming, with a growing focus on China’s debt problems and a market that has fully embraced the Fed’s dovishness, to figure out how to get outright long the US dollar again.

You can get Societe Generale FX Daily reports and various analytics from tier 1 institutions via our subscription.