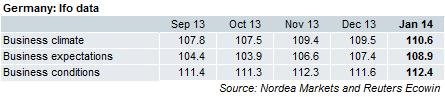

Current situation assessment up after a decline in December, expectations up again – can one ask for more? Business climate improved on a broad base, in manufacturing, in the construction and in the wholesale sector, but it slightly worsened in retail trade. Still, we expect GDP growth to be mainly driven by private consumption this year.

The surprising part of today’s Ifo report (to me, not to consensus), was the rise in expectations. Don’t trust the indications from ZEW expectations, one might say. Looking forward, uncertainty about several Emerging Marktes could dampen expectations in the months ahead. But as long as China does not disappoint, the export-reliant German manufacturing sector should do not too bad. Moreover, several euro-countries are digging themselves out of the crisis.

According to the Ifo institute, the data is consistent with GDP growth of 0.5% q/q in Q1. We pencilled in 0.4% for now. Growth seems to be accelerating, and that’s the important good message in today’s numbers. The ECB should worry a bit less.

Nordea